Disclaimer: I have a material personal interest in Macfarlane shares. A portfolio I help to manage has a large weight in Macfarlane shares. Hence, I cannot help but be biased. Please do your own research – my projections are mine alone.

Elevator Pitch

Macfarlane is a packaging distributor with 26 core sites around the UK. It stocks boxes, wraps, tape and plenty more, and sells to customers like Dunelm, Halfords and Honeywell, as well as a raft of smaller businesses.

Boring, sure – but boring is often resilient. Customers avoid managing their own warehouses full of various dimensions of packaging. Macfarlane’s scale gives it buying economies, while manufacturers avoid having to deal with hundreds of small customers. A well-run distribution business is hard to dislodge, because for every party involved, the alternative is a world with a lot more hassle. It can be mismanaged, though, as long-standing CEO Peter Atkinson found in 2003 when he took the reins of a packaging empire stretching from Guadalajara to Glasgow.

Within two years Atkinson had steadied the ship, and from that baseline in 2005, Macfarlane has grown normalised earnings from ~£1.5m to my estimate of over £17m in 2021. Accounting for dilution, that’s an EPS CAGR of 14.0%, while paying dividends along the way. A substantially above-market return.

Better yet, the return I’ve just described isn’t obvious. Non-cash accounting charges other companies would routinely adjust aren’t mentioned. Property provisions for rationalising the network – which other management teams would call ‘one-off restructuring expenses’ – aren’t broken out. That’s an opportunity, as economic earnings are more than 20% higher than reported.

But perhaps the most compelling element here is the timing: Macfarlane just announced their best H1 ever by an enormous margin. The business is firing on all cylinders as eCommerce packaging demand drives significant growth, and the recovery in the group’s core industrial business is beginning. Careful expansion into Europe provides further upside.

The market earnings multiple in the UK is around 17x. I think you’re getting Macfarlane at about 12x earnings – a big discount, particularly considering Macfarlane is a far superior business to most. It is better managed, more resilient, more predictable and its growth plans simply require ‘more of the same’. Investors are getting a winner for a discount price.

The Business

So, first things first: let’s dive into the exciting world of packaging distribution.

Macfarlane buys packaging from the big manufacturers – Smurfit Kappa, for example – and holds it in their 26 distribution centres. Smurfit doesn’t want to deal with Macfarlane’s 20,000 customers. Tinkering with delivery route optimisation and holding custom stock for rapid delivery is not their game. Hence, distribution is a win-win; it aggregates demand and reduces cost-of-service for manufacturers.

Customers – like Argos, Dunelm or Glasses Direct – place orders with Macfarlane, typically for next day delivery. These guys don’t want warehouses stuffed with huge amounts of packaging. They won’t get the best price from manufacturers compared to Macfarlane, which buys in serious volume. Nor are they experts in packaging, an unloved and unsexy part of the world of commerce. Having a consultative partner is a big help.

Of course, some big customers do go direct, and some use a mix of distribution and manufacturer. Ikea uses Macfarlane for part of their needs. But Amazon doesn’t need them at all – Amazon is big enough and complex enough to negotiate and manage their own packaging supply chain. Luckily for us, we don’t care about Amazon anyway – incessantly squeezed margins and a lopsided relationship is no way to run a business. Dunelm and Ikea are meaty customers, and even small businesses offer plenty of margin potential.

Peter Atkinson, CEO, likes to point out that the actual cost of packaging is not that material in the grand scheme of things. Think about part breakage and damages. Or the nightmare of dealing with your own packaging logistics – likely in a facility that doesn’t have the space or the layout to effectively store these materials. If you’re a growing retailer, do you want your warehouse to be stocking your £25 candles, or do you want to be stocking bulky pieces of cardboard – which you could receive as you need from Macfarlane? Like any good salesperson- Macfarlane’s pitch is to persuade the customer to see that the price is not the primary concern:

It’s important to note here that Macfarlane predominantly sells products for ‘moving goods around’ as opposed to for ‘marketing products’. Macfarlane does not stock Kellogg’s cornflakes boxes. They might be providing a big brown cardboard box in which 32 cornflake boxes are packed for shipment to a cash-and-carry. Or, better yet, they’ll sell a box and some void filling for a hydraulic pump part – because about two-thirds of Macfarlane’s business is exposed to industrial end-markets. This doesn’t mean it’s all completely standard; for most of their customers, they’ll source, procure & hold onto branded boxes, in a more consultative and value-add relationship. See this video of Lakeland, below, which highlights it nicely:

Packaging distribution has grown up as a local business. Partly this is because of the low-value, relatively high-volume nature of packaging; when you’re operating on thin margins, you can’t afford to ship halfway around the country to service far-flung customers. And those customers – whose whole operations will be disrupted without packaging – don’t want to take a risk on a supplier 200 miles away. Macfarlane spends about 3% of its revenue on logistics. For a business making 6-8% margins, that’s a material cost.

Peter has an interesting further theory as to the history of the industry, though, which I’ll loosely transcribe from this video. It’s worth watching if you want an introduction to the business:

“The reason the industry is fragmented is because these sorts of products aren’t very high profile for organisations; they’re very low on their priority list, so they often delegate to someone quite low down the food chain in terms of decision making. Their natural reaction is to use a local supplier – and because the sophistication of the way they plan and order these sort of things – like bubble wrap and boxes – isn’t very good, they want an insurance policy – and the best insurance policy is to have someone local. And hence, the industry has grown up as a series of local companies”

I find these sorts of ideas fascinating. Business structures often end up the way they do for silly, human-sounding reasons.

Anyway, the fragmented and local market is plain for all to see, and it’s a big boon for current investors, particularly if you get on board with a consolidator like Macfarlane. Packaging distribution is not a business where you want to open a greenfield site today. 6% EBIT margins are not causing competition to batter down the doors, and private equity is not fascinated by a total addressable market which probably has the potential for £75m of operating profit in the UK. It’ll take you years to acquire the customers to run an efficient distribution centre from scratch.

So you end up with sticky customers in a sleepy market without aggressive price competition and disruptive new entrants. Companies service their local areas and retain their customers unless they screw something up.

As to long term growth, there are both positives and negatives. Environmental concerns, on one hand, suggest that we should be using less packaging. Indeed, a drive to use less (for cost reasons and eco reasons) is a constant feature of the business. On the other, we are all sitting at home in an increasingly piecemeal and fragmented supply chain, buying boxes of vegetables to be delivered twice a week and mobile phone cases on Amazon. Industrial production is unlikely to get less specialised any time soon. I don’t know where this all pans out, but I am content with the assumption that Macfarlane’s end markets are flat to modestly growing.

All of this is the business school theory – the stuff they write case studies about. Luckily for us, we have actual data we can consider to get to the fundamental question we care about: is this a good business?

Financial History

Surprisingly, yes. I say ‘surprisingly’ because 30% gross margins are not software-like, by any stretch of the imagination. But when you are churning your inventory ten times a year, you are getting plenty of bites at the apple. And – more importantly – it’s highly predictable and incredibly reliable. Packaging is an unusually resilient industry because of its involvement in almost every sector of the economy. eCommerce is only exacerbating this trend. Macfarlane’s gross profit still rose in COVID-hit 2020.

Ponder that point for a second. Macfarlane faced headwinds, like all businesses. Many of their large customers are in the aerospace market, which was obviously battered in 2020. The overall level of GDP – which is typically the correlate for packaging consumption – fell by 10%. I can’t think of a better testament to the resilience and diversity of the business than the fact that profitability still improved last year.

Investors under-rate predictability, in my view. Predictability allows for effective cost management. Logistics costs, staffing costs, inventory levels and negotiations with suppliers are much, much easier when you know that demand will be there on the other side. It turns business into a game of continuous improvement – how to squeeze a little more cost out, how to negotiate slightly better prices, how to manage the network geographically. This is all much harder when you’re sweating about where tomorrow’s sales will come from.

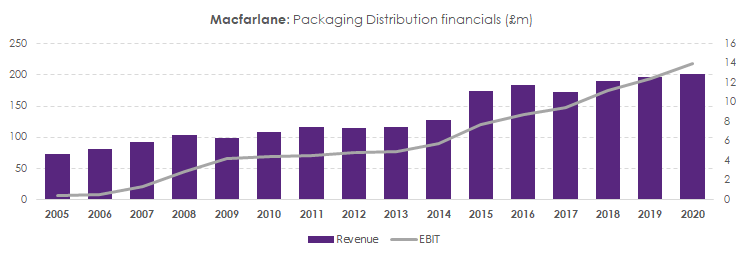

And all of that means you get a long-term financial profile that looks like this:

The dark and dreary days of the GFC are barely noticeable; the distribution business still doubled profits from 2008 to 2012. You won’t find many small-cap businesses with smoother earnings profiles than this.

It’s been profitable growth, too: the group has deployed approximately £60m of incremental capital in the last 15 years to support group level EBIT growth of ~£12m. That’s an excellent return, and as I describe later, I think that meaningfully underestimates the value creation because of the group’s conservative accounting and because 2020 figures will shortly be blown out of the water.

Macfarlane isn’t unique in this sector, either. If I look at their competitor set – other large packaging distribution businesses in the UK (all private) – we see a similar story of stability and resilience. These businesses are consistently profitable, to a greater or lesser degree, with overall average annual margins of 5.5%. That’s not dissimilar from Macfarlane historically, and a little lower than their 8% target:

The outlier in that chart, by the way – the one with margins shooting into the stratosphere – is Kite Packaging, a company with roots entangled with Macfarlane. Indeed, its formation only came about when a botched acquisition Macfarlane completed under the old management team led to the departure of a number of key executives. Sure enough, they remain a thorn in the side twenty years later!

A note on Kite and online selling (click)

Kite has benefitted from an aggressive shift to customer self-service, particularly among their smaller customers, and the expansion of their webshop. Despite Macfarlane having a substantial lead in gross profitability terms (circa five percentage points), Kite’s EBIT margin is meaningfully higher. Kite’s revenue-per-employee is the highest of all the companies I found. They are doing a lot with a little.

Judging by Macfarlane’s lesser relevance in online marketing, worse SEO, and the less-than-ideal customer journey, I believe they are behind when it comes to migrating online. I wonder if the decentralised operating structure – Macfarlane views and optimises profitability on a site-by-site basis – made it harder for them to get on board with a webshop, aggregating orders and dishing them out to distribution centres. Who would bear the burden for the investment required? How does one allocate marketing spend?

That said, I do think it’s a fascinating opportunity. I did a price comparison of a few of the websites and the variability in pricing is extreme. Kite is typically the cheapest, and Macfarlane a little more expensive, but the rest of the competition is much more expensive than either. The more aggressive brands – who are spending a lot on online marketing – are recouping it through higher-priced products. Smaller customers, it seems, are not price-sensitive for cardboard boxes & tape, and don’t do much shopping around.

This is an ‘early market’ phenomenon, in my view. It suggests a lack of sophistication around all of the players.

And this is an opportunity for growth: there is no fundamental reason that the others should steal a march on Macfarlane in the lower-touch and incrementally profitable online business. Macfarlane has national site coverage and the greatest degree of purchasing power. Structurally, they are set fair. But I wouldn’t model success. It’s hard for an organisation with its core business servicing large customers, often with bespoke boxes and consultative relationships, to compete with online-focused businesses which are pricing and marketing differently. I wonder if Macfarlane could seed an internal team as a separate eCommerce business unit, hire a bunch of folks with experience in direct-to-consumer, give them some autonomy and clear transfer pricing and let them rip.

An interesting discussion, but not core to the thesis.

Still, it’s important not to read too much into charts like this – I have pulled the data from Companies House with no knowledge of the inner workings of these businesses. Do they have similar depreciation policies? The same property structure (leased vs. owned)? Management remuneration equivalent with respect dividends vs. salary? While we can’t know that, it should give some comfort that Macfarlane is neither unusually profitable nor operating in an industry with large variability. Everyone is making money.

My hope is that Macfarlane – which is now pushing on 25% market share in the UK, they reckon, about 2.5x their largest competitor – should be able to earn margins at the top end of that group. They target 8%. I suspect if they stopped acquiring, consolidated to the operating base they’d want to work with today and ran for maximising short-term outcomes, they could comfortably beat that.

Manufacturing

One thing I have neglected to mention in the entire write-up so far is Macfarlane’s manufacturing division. I don’t think it is hugely material to an analysis of the group. In the last full year, it made £381k of operating profit – against £14.0m for the distribution side.

Granted, that was an unusually low figure – substantially below where it should be in a business segment that has hovered around £1m in EBIT for the past decade. COVID hit manufacturing harder than distribution since it relies more heavily on aerospace and other industries more severely impacted than, say, home improvement retail.

Manufacturing has two sub-segments. Packaging Design & Manufacture, while not hugely relevant from a group financial perspective, can be seen as an important facilitator of group sales. This typically produces bespoke packaging for niche or high-value products – an industrial customer needing to transport a sensitive and expensive part, for instance. Around 15-20% of the division’s sales are to the packaging distribution business.

The Labels business, on the other hand, has less to do with the broader group. It produces labels for consumer products and sells to the likes of PZ Cussons and McBride. It appears to be an OK business, throwing out a little EBIT, but it has no obvious benefit to the core distribution segment.

In the half-year just passed, manufacturing profitability improved significantly, both organically and through the acquisition of GWP. Management restructured during the pain last year, so I expect they will carry this improvement in profitability through to the full year. None of this changes my story for the group as a whole. Manufacturing is an enabler that will hopefully throw off a little extra profit. It is not core to the investment story.

Framing the Opportunity

Everything I’ve said above reiterates Macfarlane as a steady, slow organic growth business. I think that’s a fair characterisation. The flip side of packaging’s stability is, well, its stability.

But management has squeezed more juice out of this market with a consistently executed acquisition strategy. Indeed, the inorganic front has been the only operational cash consumer in the last 15 years. Organic growth has been achieved with shrinkage in the group’s PP&E. Better management of suppliers means net working capital has shrunk, too.

By my estimates, Macfarlane has spent £60-70m in the last 15 years, predominantly with internally generated cash. That spend, combined with organic growth, has produced an EBIT increase from £1.5m to £17m in 2020. This figure – the return on incremental capital – is a more meaningful statistic, and a better guide to the future than group level, point-in-time calculations. You can calculate it however you want, but I won’t quibble if you get anywhere from 15-25% pre-tax. Any number you pick in that range is meaningfully better than the average UK company and indicative of a shrewd and disciplined capital allocator at the helm.

But before we get into recent figures and the future, let’s just wrap up our review of the past by consdering last year’s financials. I hope to explain why I think the group’s reported figures are meaningfully underestimating the free cash flow this business can produce.

As I mentioned right at the start of this post, Macfarlane’s potential isn’t handed to you on a plate. In the most recent set of results, management began adjusting for the most obvious ‘costs which aren’t costs’. In my view, though, even their adjusted numbers are more conservative than the unadjusted numbers many management teams produce. Looking at 2020, for instance:

- The group reported £10.2m of net profit. No adjustments were shown. Free cash flow, on the other hand, came in at £15.9m – an early hint that things are looking rosy

- I ignore the amortisation of acquired intangibles – an accounting treatment whereby you write-off some of the value of companies you purchased. Macfarlane’s acquisitions are not depreciating in value, so this non-cash cost is accounting fiction. And this is big, at £2.5m – or ~25% of reported net profit

- The group also increased its provisions across the board. Net inventory provisions increased by £576k, a material sum on £16m of fast-moving stock. Provisions on receivables were increased by £838k, despite an aging profile which looks a little better. Property provisions due in respect of dilapidation on leased premises were jacked up by £1,766k.

Prudent provisioning is a classic sign of management conservatism – but extreme prudence on the provisioning front cannot recur every year. You cannot continually put aside much more in inventory and receivable provisioning than you write off.

Likewise, dilapidations on the exit of leased properties are, of course, a real cost. But they relate to the exit from two long-term leases, reducing the group’s property costs in the future. Each instance relates to a separate, non-recurring and long-term beneficial decision to improve the efficiency of the group. These are the costs you like paying, and they are as much ‘investments’ as they are ‘costs’, notwithstanding the accounting.

I hope my point is clear: I don’t think Macfarlane created £10.2m in economic value last year; I think they certainly made ~£12.6m, ignoring that silly amortisation. And I think we can have a robust debate about how we view the provisioning and the recurring or non-recurring nature of property adjustment costs.

Current Momentum

If you’re with me so far, I hope you agree that the company is cautious and not prone to exaggerating its virtues. You might acknowledge that the sector and particularly Macfarlane itself is stable and favourable for long-term investors. And you probably agree that, with a long history of cash earnings exceeding accounting earnings, there’s more to Macfarlane than meets the eye.

Hence, one might conclude that 2021 would produce another solid but unspectacular performance, continuing a long history of not surprising investors.

You would be wrong; because H1 2021 was a brilliant six months for Macfarlane.

Operating profit doubled on revenues up 26.5%. Indeed, EBIT of £11.1m was approximately 72% of full-year forecasts prior to the release of this set of figures.

Brokers have raised forecasts – but H1’s profit is still 51.3% of that fresh figure. Even if the group had no seasonality, that would be a harsh assumption, I think. Macfarlane completed two acquisitions this year, and they came partway through the first half. The simple mechanical effect of a few more months of contribution from those will add a few hundred grand of profit.

But, more importantly, Macfarlane has historically displayed a pronounced H1/H2 split:

Now, there are some clear reasons for caution. Input prices have been increasingly aggressive, and Macfarlane will need to manage its customers carefully to effectively pass on these price rises. One other thing I haven’t quite figured out is how their two newly acquired businesses contributed £1.9m of EBIT in the few months they were owned. It’s much more than I was expecting. And the industrial recovery is yet to properly come through in the numbers, which is both a negative and a positive in that it leaves a little upside on the table for the next couple of years.

Perhaps this year will be the first in Atkinson’s tenure that H2 is weaker than H1, which will be necessary to meet market forecasts, despite the obvious signs of very strong trading. I don’t think it will be.

Tying it Together

The reasons I find Macfarlane so exciting today also make the business difficult to forecast.

We have never seen an H1 performance this strong before. That makes it hard to know whether it augurs an exceptionally strong H2, or if the existence of such an anomalous event should make us more cautious as to our predictions.

Likewise, conservative accounting means I am directionally comfortable with earnings figures, but it also makes things hard to predict. I never want to make blanket assumptions that management are overprovisioning, and start to adjust or assume that’s the case. That feels dangerous to me. So I would rather comfortably sit in the knowledge that profits are always likely to be cash-backed, and that the accounts are simply a prudent reflection of the truth.

Still, we have to try and put something on paper. Here is my current best guess for where FY 2021 will pan out:

I hope I’ve made my assumptions fairly clear in the table above. I will reiterate that these forecasts contain a wider band of uncertainty than usual: on the one hand, you might consider that assuming Macfarlane will have its first-ever H2 margin reduction is punitive. On the other, you might think that assuming 10% organic growth is aggressive given much stronger comparators than in H1. I look forward to any and all debate in the comments!

But let’s say you agree with me, and think they’ll earn ~£17m this year. This puts them, at the time of writing, on a P/E multiple of 12.4x for the year which will soon end.

What’s a fair multiple to pay for Macfarlane?

Well, multiples are simplifications of proper DCF analysis, and you can distil down to two things: how fast is a business growing, and how safe is the business? Safer – more ‘bond like’ operations, with smooth cashflows and little variability in results, deserve a higher multiple. Likewise, businesses with the opportunity to grow – either organically or acquisitively – also deserve higher multiples.

How does Macfarlane stack up?

Let’s take the latter first; the growth. Macfarlane is manifestly not in an explosive market. But – through consistent organic improvement and a repeatable and reliable acquisition strategy, they have grown at mid-teen rates for a long period of time. The ‘follow your customer’ program, moving cautiously into Europe alongside customers they know and trust, is an increasing focus of the group. And the pension deficit – which had been a millstone around the group’s neck for the last decade – is no longer an issue. I think Macfarlane can continue to do what they have been doing and continue to get a little larger and a little better every year.

And as to the first factor, stability, I don’t need to reiterate what I’ve said above. If market fundamentals don’t persuade you – crucially, packaging’s relevance to every sector of the economy – the financial track history of the business should. Investors recognise this in other packaging companies, which trade at full multiples.

The market multiple at the moment is somewhere between 16-18x. In my view, Macfarlane’s clear and executable growth strategy and the defensive nature of its business means it is certainly a more worthwhile investment than the average company. Hence, I think a 180-190p price target for the company is both realistic and achievable, likely after the market wakes up to how well they are trading.

That said, it’s not how I think about valuation. Every business I buy, I intend to hold for many years. Hence, I mostly think in terms of expected return, not point-estimates.

With the pension deficit issue behind it and a balance sheet with only a little net debt (which is being paid down rapidly), Macfarlane is set fair for the medium term. I wouldn’t be surprised if we see an EPS CAGR in the low-teens, combined with cash returns of 2-3% annually. That gives me an expected return in the mid-teens, with lower risk than the vast majority of other investment cases I see. Given the investment landscape today, that’s compelling.

It’s a long way from sex, drugs and oil & gas exploration, but I think Macfarlane makes a great bedrock to a portfolio.

Great write-up. What changed so that margins have almost 2x in the past 2 years from historical levels? From 2005-2014, EBITDA% averaged around 4%. Sales only grew at ~2-3% and there was no evidence of oper leverage. Seems really attractive at the current margin structure, not so much if business is at a Covid/e-commerce “peak” that will get whittled back down. Not saying it is btw, but seems like the risk. Any thoughts?

I agree with your overall point, even allowing for the IFRS16 adjustment you mention in another comment – you need to add that back in as it really skews the historical comparison. I would simply look at EBIT margins since the economic depreciation structure hasn’t changed too much and it makes for a simpler long-term series.

Broadly, you will see that the EBIT margin improvement over the last 15 years has been a continuous march upward: and that it continues more or less insulated from fluctuations in the gross margin line.

I think the point you mentioned – the chance of a reversion to historic margins – is a key risk, and frankly I don’t have an excellent intuition or understanding of how or why margins have improved so continuously beyond vague notions of ‘scale’ and ‘efficiency’. Unsatisfying, I know. There are lots of little things you can consider:

– Europe went from being an EBIT loss/breakeven ten years ago to more consistently profitable now

– Acquisitions have tended to have higher, sometimes meaningfully higher margins than the existing group

– Greater support for the fairly high listing/public company costs (they are fully listed) on a larger group profit base

– Much business is now transacted online, with no erosion to gross margin. Revenue per employee has hence risen (though not dramatically)

I would note that if there is a ‘peak margin’ environment for Macfarlane, the current one probably isn’t what one would expect. The bulk of their business is in industrial end-markets still impacted by COVID, and the eCommerce strength partly ameliorates that but does not solve it completely. They had to deal with significant pricing inflation in H1, and H2 will be a better test on this front.

Ultimately I think the margins are just something you have to take a view on, with a little fan chart in your mind. I assume they will remain around these levels. I am open to people who think I’m being very aggressive, and who would prefer to assume they mean revert. I’m also open to the view that, with scale, dominant market share and improvement almost every year for the last 15, I should be modelling still ongoing improvement.

* Forgot to mention: IFRS16 is part of it w/ lease depreciation now being added back, so not quite as dramatic but overall point still holds I think..

Thanks Lewis. Fascinating write up. I wonder if you could expand on why it is reassuring that MacFarlane doesn’t look especially profitable for a packaging distribution business? I guess I would be looking for a business that was more profitable than peers..

Thanks Richard. Fair point. I came at it with a pessimistic hat on – “is this business making too much money? Should its margins mean revert?” and an analysis of competitors suggests to me that no, not really, it’s not especially different from its peers, and the sector seems resilient. They make unspectacular but positive margins across the board.

I agree that Macfarlane being better than all of its peers is a question on which the jury is still out. Margins have improved essentially every year for 15, and will improve again significantly this year. They will not be as strong as Kite, but they will be very strong. I’d love to look at Kite if it was listed, but alas it is not!

Hi,

What do you see as the growth drivers going forward given they have already reached 25% market share in the UK? If the drivers are outside the UK, are the markets / their chances of success comparable?

Thanks

Hi Alex,

Three pillars:

– Firstly, there is probably 0-3% volume growth in the market, so maybe 2-5% nominal with pricing growth. This is the baseline.

– Secondly, despite their large market share, I suspect they will be able to continue to growth in the UK. They have completed a couple of acquisitions so far this year and indicate they want to do more. I have no idea if the CMA would ultimately have any interest in business-to-business packaging distribution…

– Finally, they will almost certainly expand into Europe, and this is obviously more risky than the rinse and repeat acquisitions they have been executing in the UK. There are a couple of reasons it’s not a complete punt, though. Importantly, their customer and supplier relationships are very valuable even overseas – indeed, their ‘follow the customer’ program has them already operating in Europe, albeit using third party logistics (so they don’t own the real estate and fleet). Indeed, they did £10m of European revenue last year at a healthy margin. I take some comfort from the fact that they have been operating in Europe for years with a low-risk, low-capital investment model, and after having learnt the ins and outs they will acquire the infrastructure and build it out more robustly. This seems sensible to me.

I don’t think you need very strong growth to get a good return here. If they meet my targets for 2021 earnings and grow a little annually from there, I suspect the resilience of earnings will at some point be recognised by the market and cause a re-rating to at least a ‘market’ multiple. Growth will be juice on top.

Best,

Lewis

Hi Lewis, great write-up on a business that had so far escaped my attention. I was wondering if they have they ever articulated how they think about capital allocation? Whilst their acquisition strategy is very Bunzl-like, I noted they had issued shares in several years to do acquisitions, and Management don’t have big shareholdings and are only partially remunerated on EPS. Also, whilst the distribution business is clearly more attractive, they have just spent £15m on a manufacturing business, albeit bespoke design so more value-add, but is this a sign for eg that they are having to offer more capital-intensive manufacturing in order to serve customers. I think they are also incurring capex for equipment for the label business too but do not seem to address whether this is a good use of shareholders capital. I guess I am trying to get a handle on whether they get that it is not just the earnings power they generate that is important but the quantum of shareholders’ capital they have consumed to generate it. Thanks very much for highlighting this business.

Hi Jerry,

Thank you – all excellent observations.

I wouldn’t say they have articulated a clear capital allocation ‘philosophy’, so I think the best one can do is infer from their actions… which is sometimes better than a stated strategy, anyway! To take your excellent points in order:

– I would love if management owned more. That said, I am never a fan of overly generous LTIP schemes. This is always a bit of a quandary when it comes to non-founder executive management teams, who come in with no equity and typically don’t have the wherewithal or desire to invest seven figures… in this case, I simply live with it, instead relying on the fact that Atkinson has executed so well to date. I think he’s intrinsically motivated by ‘doing a good job’.

– They have issued shares; I would also rather they had not. I hate dilution. That said – the pension deficit was a very pressing concern in the early to mid 2010s and debt peaked at 1.5x EBITDA. Not a huge issue in isolation, but a sizable actuarial (and smaller accounting) pension deficit combined with a debt burden in a small cap business is toxic. I don’t think they could’ve credibly financed their acquisitions with more debt, so they had two options: don’t do the deals, or do the deals but dilute. I think the earnings performance in the last five years suggests shareholders should be happy that they incurred some dilution for a meaningfully stronger business as a whole.

– I am on the fence with respect to the manufacturing acquisition. To management’s credit, performance since acquisition has been spectacular – implying they have likely acquired it for a very low price. There is also perhaps some small argument that, as distribution grows, there is more capacity to support an internal manufacturing business with demand. That said – I describe manufacturing as a service provider to the group and a facilitator of sales in my own write-up. It would be hypocritical if I now espouse the virtues of expanding that segment. I plan on discussing this in more detail next time I see management, and see if I can be persuaded that manufacturing is an attractive outlet for capital investment in its own right, or whether this was just a ‘great deal’.

– I get the sense that the labels business is non-core, and I don’t think the printing press was that substantial an investment – manufacturing investment in total over the last ten years pales in comparison to that in distribution – but your point regarding capex stands. Indeed, it is even more pertinent if the labels business is not a long-term pillar of the group.

The question I ask myself regarding manufacturing is: “what would it take for me to change my mind?”

If labels can be disposed of and/or the manufacturing group as a whole starts to show consistent profitability improvement at a high return on invested capital in the coming years, then I will reassess my gut feeling that Macfarlane should be solely focused on investment in distribution. The challenge is that manufacturing profitability has been unreliable and prone to swings. Trust in management is required here in the interim. Still, given their track record I inclined to give them the benefit of the doubt.

– I would say that their discipline with respect to acquisition pricing suggests that they are well aware of the importance of prudently deploying shareholder capital – they typically know these businesses for many years, and buy them for a fair but not full multiple. This is not a ‘splash the cash’ approach based on whatever a broker throws onto their desk. I would also say that their tight management of working capital is not indicative of a management team focused solely on profitability to the detriment of capital employment.

Thanks for the additional insight Lewis. On the manufacturing., it’s not abnormal in my experience for value-added distributors to do some assembly or bespoke manufacturing and this can often be quite lucrative, so this may well be the idea with GWP, it would be interesting to hear what Management have to say about that. Best regards

Agreed. I used to hold Solid State, which had a value-added distribution arm and a manufacturing arm. It’s completely different, but the same intellectual leap takes place there – as a distributor you quickly realise there are business problems you can solve for your customer by doing a little more heavy lifting, and before you know it, you are manufacturing sub-components or systems and delivering them whole, taking another thing off your customer’s plate.

Hi Lewis, I saw they are selling the Labels business. This certainly removes part of the question mark I had articulated above regarding capital allocation as I couldn’t understand why they were putting capex into this. Didn’t necessarily kill it for me – S&U for example had a legacy hosiery business but Anthony Coombs shut it pretty quickly on taking over in early 2000s when it started deteriorating rapidly. So, this definitely moves Macfarlane up the DD list for me. Thanks for highlighting it.

No worries. They got a decent/good price and simplified the business so it’s a clear win in my book.

Hi Lewis,

I read and then recently re-read this write up, I think it’s fantastic so thank you! I had a few questions, if you don’t mind:

“assumption that Macfarlane’s end markets are flat to modestly growing”: Where does this assumption come from? I would of thought it is rather conservative, which is no bad thing, given ongoing structural e-commerce growth. And is there the possibility that a trend towards reducing packaging might mean more sophisticated packaging, possibly where Macfarlane’s can add value?

The latest German acquisition looks little more expensive than others at nearly 10* EBITDA. Do you have any thoughts on this and can you talk me through what sort of existing Macfarlane’s customer would benefit from this German acquisition.

Many thanks again for the initial idea.

Timothy,

That’s kind, thank you.

Regarding your first point – my market growth assumptions – I agree, it may be conservative. But I find it hard to gauge. There are a few factors pulling in different directions:

– POSITIVE: Packaging has tended to grow with GDP (as economic activity increases, more stuff moves around, which requires more packaging)

– NEGATIVE: That said, the world is demanding a reduction in packaging for environmental reasons, so everyone is trying to minimise use wherever they can. Companies have teams looking where they can cut packaging volumes

– POSITIVE: This might be an opportunity, not a threat: less packaging, but better engineered, will probably cost more than simple but very large boxes (a la Amazon!)

– NEGATIVE: Are we at ‘peak stuff’? That historic GDP trend has held, but increasingly spending is being diverted away from buying more ‘things’ and toward the service economy. How much stuff do people need?

I don’t know where it all pans out. It’s certainly not going to grow at 8% per year, but I also think it’s unlikely to shrink 2% per year (by value). I wouldn’t really argue if someone has a view anywhere within that range.

Regarding the German acquisition: it does look a little expensive to me, too. That said: when making your first proper foray into an international business, I think the single most important factor is locking up the highest quality and most resilient business you can find. You should be risk averse and less concerned with valuation. The consequences of having a poorer quality business – which may require restructuring or high levels of management team – are disastrous abroad. It’s certainly a risk factor, but international expansion is also the biggest opportunity for the group. I can’t really say anything at this juncture beyond the fact that I trust Peter Atkinson and think he’s an excellent CEO. It might go wrong, or it might unlock the next leg of the Macfarlane story.

I would note that they are paying EUR6.9m up front for the EUR0.9m of EBITDA, so approx 7.7x EBITDA. The rest of the consideration is earn-out, contingent on future profitability. So it’s a little cheaper than you are seeing it.

Regarding what it does for Macfarlane’s existing customers – only a little bit, on the margins. To the extent existing customers are also present in Germany, Macfarlane can service them there. Some of them might avail themselves of this opportunity. But mostly, Macfarlane is acquiring a new customer base in a new market where they will hope to repeat the buy-and-build success they’ve had in the UK. I would view them as largely separate businesses, just with shared expertise.

¡Hi Lewis!

Brilliant post. I agree with all things that you said. In my opinion it’s a good idea to replicate the same UK model in Europe and try to expand the Group. Atkinson demonstrate to be an encourage person.

Also I want to highligh the good investing that you realized with the results of the first and second half year results.

My questions are the next ones:

– When you value the Macfarlane company, to make an investment decision, which ratio de you use? PER, Market Cap/FCF or EV/EBIT?

– What do you think about the less “skin in the game” by part of the Directors? It’s true that Atkinson demonstrate that have good CEO’s skills during these period, but it worries you that the lack of shares in the director’s group?

It’s a pleasure to me can read this kind of articles. You realized a nice job. My congrats.

Gerard Martinez

Thank you, Gerard, that is very kind: and sorry for the slow reply.

I think it is probably easiest to value Macfarlane on a P/E basis. Accounting is fairly straightforward, so without acquisitions, earnings should be quite close to true free cash flow. In a normal market I think Macfarlane is probably worth 14-16x earnings, though everything in the stock market is obviously relative so P/E targets are always very subjective. Suffice to say I think that, at the current price, it is a much better company than the broader market at a cheaper price than the broader market.

I would love if Peter Atkinson owned more shares. Alas, he is not a founder, and evidently over the last 20 years he did not want to buy aggressively. I find that a little surprising – he is an entrepreneurial guy – but you can never really know someone’s motivations. Perhaps he thinks that he has enough of his life tied into Macfarlane, given it pays his salary, without having a big investment in the company too. Ultimately share ownership is a good indicator that someone will have an ‘owner mentality’, and a good sign that they might be aligned with shareholders. In Peter’s case, he does not own many shares, but I think he nonetheless mostly thinks like an owner and treats shareholders well. So I am relatively comfortable.

Best,

Lewis

Hi Lewis, I was wondering if, in light of recent softer data from Macfarlane (specially on the distribution revenue side) you have changed your mind in any of the assumptions that you previoulsy made on your brillian Macfarlane thesis almost 3 years ago. Personally, I have been following the company for some time now and I would argue that since then, (i) the risks of the environmental legislation impacting the business in the future have increased a bit and (ii) I see competitors a little bit more agressive than in the past (Kite packaging for example). I still see the company as a great opportunity but I guess that I would be more conservative on the eps growth prospects (from +8-9% to 6-7%) and P/E exit multiple (from 15x to 13x). Thanks a lot,

Hi Oleg,

Thank you: the comments you make are entirely fair. Environmental concerns are accelerating, which will be a bigger headwind on the volume side than I had appreciated before. Kite Packaging is continuing to do very well, and represents a meaningful competitor.

I do think that – as is always the case – there is a natural inclination for folks to overemphasise the challenges in a poorer market environment – ‘price drives narrative’ and all that. I suspect Macfarlane’s volumes are cyclically at a low point, and in combination with pricing declines we have a soft performance in H1 which will likely continue into Q3. In hindsight, COVID represented a boom in demand for packaging, particularly through e-commerce, and we have spent the subsequent years operating against a big volume headwind to get back to a ‘trend’ level of consumption. I think that is now done, but I can’t be sure.

Hence, disentangling the secular risks from the cyclical ones is a challenge. The current price would suggest that the market thinks Macfarlane is either ex-growth or will face significant margin declines. I’m not so pessimistic. If one was being bullish, one might hope that a more complex packaging environment – with more taxes, more legislation and a greater variety of options with varying benefits and drawbacks – would actually benefit a consultative distribution partner, particularly against their local ‘box-shifting’ competitors.

I’m not sure I’d go that far – I don’t think being disrupted is ever really a ‘good thing’ – but I do think the pace of change is slow enough and packaging is important/sticky enough that none of these challenges are insurmountable.

Organic growth was never a hugely important driver of my assumed EPS growth in the medium term. Given low historic organic growth, the vast majority of their success has come from acquisition. The ability to acquire businesses cheaply and integrate them well is hence much more important to future returns, and I haven’t really changed my view there.

In sum: yes, I would trim back growth expectations. It’s hard to do that without also saying that the P/E should be lower. I don’t really enjoy debates about appropriate P/E ratios because it’s so context dependent, but I would argue that Macfarlane is a much more stable business than average, with good routes for re-investment of capital by a team which has executed exactly such a strategy successfully before. I hence think it is better than your average business, even with some headwinds to organic growth. Thus, I think it is certainly worth a premium to the stock market as a whole, and depending on your risk appetite, perhaps a significant one noting its resilience in a range of economic environments. It’s a real stalwart.

Best,

Lewis

Hello Lewis. Hope you are doing well. What are your thoughts on Macfarlane’s profit warning? I ‘can’t recall a worst printing by the company. After speaking with the managment, they claim that this results are caused by a couple of factors at play: 1- Deferral of business from H1 to H2 due to economic uncertainty plus 2- extra costs (rents and national insurance). Together, these. two effects brought Ebitda down -17% aprox in H1..

I am not sure if this is a “one off” or something more structural is going on here. The company claims that there are no structural issues going on, such as competition or client churn. But the truth is that the company has made a lot of M&A the last couple of years and its Ebit will be lower. in 2025 vs 2022. I like the business and think is well run but I dont know if I am missing somthing here? Thanks

Hi Oleg,

Sorry for the slow reply to you, too – please see my notes to AVI, below!

I think we’re all chewing through the same thing – and the market more broadly is wrestling with exactly these questions. How much is structural, how much is cyclical, and how much – after you posted your comment! – is truly one-off with the tragic accident at Pitreavie?

As I mention below, I think the economy for Macfarlane is far worse than the broad headlines would suggest. But one can’t be entirely uncritical – they must’ve lost share to Kite (and others) and costs have continued to expand. Many of those costs are outside of their control, I note, but it’s still an uncomfortable situation.

I wouldn’t like to be too confident. I think the only intellectually honest thing one can do when one has been wrong is to say “I’ve called it wrong in the past, so I should treat all my views here with a high degree of uncertainty”. That’s essentially where I am.

What do you make of recent challenges? Agree with your initial thesis here – this seemed to be a much more stable and conservatively run business, but boy 2025 was a big reset. They finally instituted a buyback but went right on buying ahead of the huge profit warning and tragic worker death, which seems like strange capital allocation. How much of recent challenges are due to economy vs. competitive pressures (Kite for example seems to be done much better). How do you think about normalized margins after the reset? And does it deserve to trade above 10x P/E?

Hi AVI,

Sorry for the slow reply. I agree – the buyback looks a little strange. I can hardly disown it now because I was vociferously arguing for it at the time, but I reflect that very often the final impetus to actually initiate a buyback comes when a business feels on the back foot, like they ‘should be doing something’. I don’t know if that’s the case here, but you could see how an outsider might view it that way.

I certainly underweighted the impact of legislation and environmental pressures, which have been a big headwind to growth. I also think I underappreciated how relevant it is that while, yes, the UK is ‘growing’ – the physical economic over here is certainly not growing, and is shrinking at pace. Broad statements like ‘Macfarlane is a stable business tied to the overall level of GDP’ are an oversimplification in an environment like this, where the only sectors growing are government spending and broader services.

Macfarlane are experiencing cost inflation while their end market is slowly but persistently shrinking. It is also hard to argue that Kite isn’t continuing to take share.

My gut says we’re near the trough on sentiment terms. Broader macro improvement would flow through quickly, and I do think they have lots of cost levers they can pull but didn’t need to in the good times. I still think it’s certainly a >10x P/E business through the cycle, but even their comp set has brutally de-rated (Bunzl now on 12x) so one shouldn’t be too uncritical…