Disclaimer: I have a very material personal interest in S&U Plc shares. A portfolio I help to manage has a very large weight in S&U Plc shares. Hence, I cannot help but be biased. Please do your own research – my projections are mine alone.

Elevator Pitch

I’m a firm believer that, if your stock idea is a solid one, you should be able to explain it in one minute. No bells and whistles, no complications. So here goes:

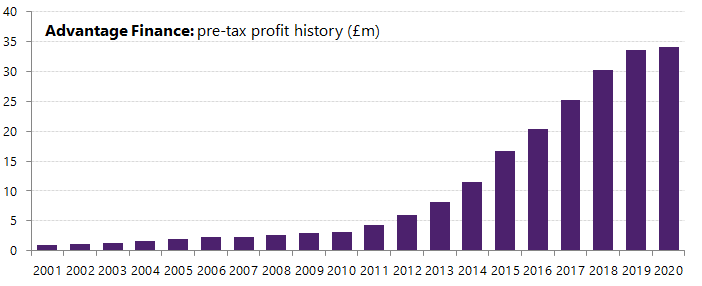

S&U is a financial holding company with two divisions. The dominant one is Advantage Finance, which lends money to car-buyers with imperfect credit histories.

This is an inefficient and hands-on market: you have to actually price for risk and be selective with borrowers. But it’s also very lucrative: since foundation in 1999, Advantage has grown profits every year at a 20%+ clip. Return on capital over the last decade is consistently 16-17%.

Management and their families own half of the outstanding shares, and you can tell from the way S&U is run. The company is fair to its customers in a space where many are not, and the balance sheet is conservative. Their 18% annual total shareholder return over the last two decades is not built on leverage, but on underwriting quality. And – no surprise – they reward shareholders with large dividends, even while the group is growing.

You get all of this at a 7.3x historic P/E, or a smidge over net asset value. This year will be tough – earnings will halve, driven by big, one-off provisions – but the group is then set to rebound and carry on its prior trajectory.

My assessment is that business growth and dividends will drive a 13%+ annual return for investors here, even if S&U were to stay at their current miserly multiple. Those are the investments I love: companies which are fundamentally creating value every year and are cheap to boot.

And why is it cheap? Simple, I think: no broker covers it with any attention, it’s too illiquid for most institutions, and most private investors (rightly) shy away from financials. S&U gets lumped in with the rest, when it’s a diamond in the rough.

Yeah, yeah, I know what you’re thinking. “You must be a bloody fast talker to fit that into a minute”. Luckily, I am.

Advantage Finance

Let’s go into a little more detail on the key division I mentioned above – Advantage Finance.

Advantage Finance is a provider of non-prime, hire purchase car finance: they help people with imperfect credit records buy used cars. They lend around £6,500 on a typical deal for about 4 years. The customer makes a fixed monthly payment and ends up owning the car.

If you’re already dragging your cursor up to the top right of the screen to close the window, give me a little more time. I also hate investing in financials: they’re opaque black boxes. Trust me when I say – like you told your first girlfriend – that S&U is not like the other guys.

Here is why it’s worth giving them at least a couple of minutes: