Disclaimer: This is not investment research, and you should not consider it as such. It is commentary based on publicly available information. I have a very material personal interest in Quixant Plc shares. A portfolio I help to manage has a very large weight in Quixant Plc shares. Hence, I cannot help but be biased. Please do your own work – my projections are mine alone.

Introduction

Quixant isn’t my usual type of investment. I tend to like non-cyclical businesses with very consistent earnings growth. I try to minimise the probability of negative surprises. Quixant doesn’t tick those boxes: its key division relies on a cyclical end market. It has, in the last few years, been beset by woes both market-driven and of its own making.

So if you’re looking for something safe, assured and consistent, you’ll probably prefer my posts on Macfarlane and S&U.

But if you’re willing to look past the scars of the last two years, let’s discuss Quixant Plc. It’s the only example I have in my portfolio of a real turnaround: the one case where I have enough faith in management to back them to come out the other side bigger, stronger and better.

Elevator Pitch

Quixant is an engineering led manufacturer. The bulk of the group’s profit comes from one vertical – gaming.

For this, Quixant produces computers powering the slot machines you will see in Vegas and around the world. Slot machine manufacturers recognise that the key to selling slots is writing compelling games. Building the physical PCs, and getting them through a lengthy regulatory approval process, is a tedious necessity.

So, they partner with Quixant, to our great success: from 2010 through to 2018, the group grew profits from ~$0.6m to ~$14.6m. The market loved the story, and the shares traded at almost 30x earnings.

Since then, though, we’ve had two major setbacks. The first was self-inflicted. The company had a heavy dependence on one customer which lost significant market share. The group failed to grapple with the size of the issue, and repeated profit warnings blew investor confidence.

The second was market driven: COVID. Slot machines represent discretionary and deferrable expenditure. Unsurprisingly, with the world’s casinos closed, Quixant’s customers turned off the taps: and it made a loss for the first time in its listed life.

So far, so gloomy. What is there to like?

Well, perhaps the last three years are not the best guide to the future. Perhaps we can look through one internal stumble and a big market implosion. Maybe Quixant is still a brilliant business underneath it all, trading at ~8x peak earnings.

Quixant has gained customers in this turmoil, and embedded itself deeper in existing ones. It is back making a profit in a very difficult supply environment, and I reckon they are at their highest ever level of order intake. I rate management and their conservatism exceptionally highly. I also think there are signs that they are managing to become relevant in markets outside of gaming.

There is a wide spread of outcomes here, but Quixant has all the ingredients to be a much bigger – and more profitable – business. If they execute, prior peak earnings may be a long way in the rear view mirror.

The gaming business

Quixant’s core business is gaming. It accounts for a large majority of profits in a typical year.

The genesis of Quixant came when the founding team were working together at another electronics business, Densitron. Their discussions with customers led them to a gap in the market: ‘all-in-one’ integrated computers for the gaming sector. Unfortunately, the Board reception for their pet project was rather lukewarm. So they backed their instincts, and left to create Quixant.

The pitch to customers is simple. Slot machine manufacturers don’t want to be developing hardware. It is not core to what makes a difference to their customers: the casinos. The ‘fairy dust’ is the game’s probability logic, which dictates odds and payouts. Get that right, and you’re golden: it’ll hook people in with the classic slot machine feeling that the win is ‘just around the corner’. The graphics and presentation of the game are also important: both internal and external. Fancy graphics on screen and a slick looking and bright cabinet will give the right first impression.

But the computer which runs the game, and the drivers which stitch together the various functions (bill accepters, regulatory modules) are irrelevant. Punters don’t see it, and casinos take it for granted.

The below chart has been in Quixant’s presentations for almost a decade, and it sums up the value proposition:

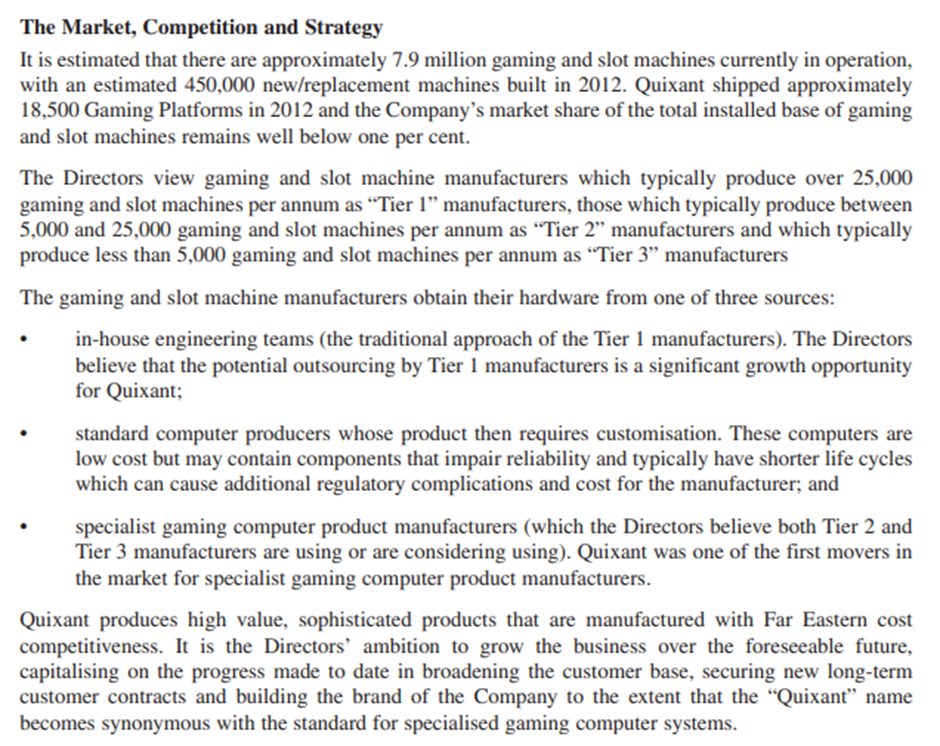

The admission document is still a great primer on the company. Not too much has changed, so I’ll reproduce the section on ‘market, competition & strategy’ in full below. It lays out the pitch which drove the stock for the next five years, seeing the group ten-bag from its IPO price of 46p.

Quixant’s 18,500 gaming platforms shipped in 2012 became 61,000 in 2018. Revenue growth led to solid profit growth, peaking at $14.2m.

I think this is a solid and defensible business. Owning a non-core, finicky but integral component in a bigger process carries benefits. Switching costs for customers are high. In Nevada, a key jurisdiction, a regulator must approve every supplier and component change. Even without that regulatory barrier, manufacturers are always hesitant to change providers of key components unless you have really screwed up.

All of this combines, in Quixant’s case, to create an end-market trajectory which has been one-directional. I believe the company has never lost a customer of any real size. Companies which outsource to Quixant, reassigning their in-house teams as a result, do not go backwards. And there are no real, dedicated competitors to Quixant. The volumes they produce are so small as to not be interesting to the large computer manufacturers.

So the obvious question is: if it’s all so great, what happened?

A bucket of cold water

Well, 2019 happened.

Up until 2019, Quixant had been walking on air. They were winning new customers and their existing customers were growing. Every year was better than the last.

As often in life, success breeds complacency. I think Quixant got complacent. The business – which was accustomed to growing order volumes – had no intelligent forecasting function. They had ridden a powerful wave off the back of their largest customer, Ainsworth, which was now heading into trouble.

See, slot machines are like any media business: hit driven and mercurial. Aristocrat Leisure’s ‘Lightning Link’ had cracked the code. There’s an article which walks around the edges of it here, but suffice to say Lightning Link was taking over Australia, and before long, the rest of the world. Look what it did for Aristocrat’s profits!

Alas, where there are winners in business, there are losers, and Ainsworth was losing out big time. Ainsworth’s public reports suggest that sales fell from almost 11k units in 2017, to ~10k in 2018, to ~7k in 2019. Quixant supplied all of Ainsworth’s computers, and Ainsworth’s own orders were drying up.

The first hint of trouble came in Quixant’s 2019 final results, which noted that:

During the year we experienced softer than anticipated demand for our platforms from some of our key customers. Overall market conditions have normalised during 2019, although some of our key customers have indicated to us that their demand for our gaming platforms will be more second half weighted than previous years, and we consequently anticipate our performance to mirror this trend. In light of this, we are taking a modestly more prudent view of our anticipated revenues for 2019

But in September they dropped the hammer:

“… new information from some customers regarding order levels for the remainder of 2019 indicates that, while this second-half weighting will occur, due to lower than expected demand for our customers’ gaming machines, Quixant’s total revenues will be below previous expectations and consequently will result in a reduction in full year profits for the Group to between $12.0m and $13.0m.”

And in January the miserable run was compounded with another profit warning:

“The Board expects to report revenue for the year of $92.3m and adjusted profit before tax of $10.7m. The majority of the shortfall against expected revenue has been experienced in the Gaming Division which has had a consequential impact on profit.”

This took the sheen off the Quixant story. The shares – which had been beloved at 30x earnings – fell ~65% to £1.65.

Kicking a man when he’s down

This takes us to March 2020. The now bruised and battered Quixant was working to regain investor confidence and put a baseline level of profitability beneath it.

You don’t need me to tell you what happened in the ensuing months.

Quixant was hit much harder by COVID than most. The complete closure of most of the world’s casinos meant that slot machine orders slowed to a trickle. Quixant reported that the gaming division had seen ‘minimal orders’ during the three month lockdown period.

Management were incredibly forthright with the issues they were facing. Two companies stick out in my mind for their approaches to handling COVID communications. Belvoir was one, and Quixant was another. Quixant laid their entire hand out on the table for the world to see. There was no bullshit and no sugar-coating. Look at their scenario planning:

The Board’s central case scenario is based on the existing debts being recovered, irrevocable sales orders already received from customers and their related costs of sales being fulfilled, and an assumption that we will only recover 50% of debts from these new fulfilments. Under this scenario, the Group would have sufficient funding to pay existing overheads without reducing them until the second half of 2021. The analyses depend greatly on the amount of orders assumed to be collectable in cash, major changes to this could significantly change the result. In all scenarios considered the Board assumed that the Group’s medical sector revenues did not stop, including revenues from displays sold as components for ventilators.

The Board’s severe downside forecasts are based on a scenario where customers stop paying entirely for new orders delivered from April 2020 onwards and do not begin buying any further goods until December 2020. Orders delivered and invoiced up to the end of Q1 2020 are assumed to be paid for. Cost reductions can be made to offset this reduction in cash receipts by a 25% reduction in staff costs and a reasonable reduction in other controllable costs. The Group have a $3.0m loan facility in Taiwan that is currently undrawn and is part of the mortgage on the Group’s property in Taiwan. In this scenario, the Group have sufficient cash until March 2021 without drawing on its bank facilities. The Board therefore consider that the Group’s strong balance sheet and material net cash position means it is well positioned to navigate through the impact of COVID-19.

In the negative case, they assumed an 8-month period where they receive no orders. They modelled that Quixant would continue fulfilling existing sales obligations without payment. They also discussed a four-phase plan, talking through the various steps they would take to conserve cash. These varied from ‘mitigate low impact cash commitments’ at the low end, to ‘widespread cost cutting to limit overheads, accepting material damage to business operations’ at the top.

This is proper downside planning, forthrightly communicated with shareholders.

Fortunately for all, it was never that bad. I still think we should appreciate a Board which respects its shareholders enough to provide them with the unvarnished truth. The share price was down 86% from its peak at this point. Many would be tempted to apply a liberal layer of gloss.

The time between then and now has been a period of recovery for Quixant, and gathering momentum.

The question you have to ask yourself is what the last two years mean. The first year had internal challenges, while the second saw external ones. Is this indicative of a once brilliant company, now permanently off the rails? Or is it an opportunity to get a tarnished – but intact – gem?

Today I think this question is particularly pertinent. Chastened and not wont to set themselves up to fail again, management have yet delivered three statements in a row hinting at very strong trends bubbling under the surface. The stars may be aligning.

But before we get to that, let’s briefly discuss that management team.

Management

With the wonders of modern technology, you can form your own initial view of management without leaving your chair.

Johan Olivier, CFO, is relatively new to the whole set-up, though you will find him on recent Investor Meet Company and PI World presentations.

Jon Jayal, on the other hand, is an old hat. He was part of the founding team and helped to design Quixant’s first products. After a brief stint in finance he returned to the business as COO in 2012. In 2018, he took over as CEO.

I have had the pleasure of meeting Jon many times over the last 8 years. As I mentioned when I discussed Macfarlane and S&U, it’s hard to write something to try and convey conviction in people. It is subjective.

But, as I have said elsewhere, forming a view is vital. Here is mine.

Jon is not a BSer, which alone makes him better than 70% of small-cap CEOs. I think he is highly competent, straightforward and honest. The issues in 2019 were regrettable growing pains, but I think in a world without COVID, Quixant would have found its feet again. Underneath the conservative exterior, he is ambitious with respect to what Quixant can achieve. I also take comfort from the fact that the rest of the founding team – who still own a third of business between them – place their faith in him. They know this business inside and out. It is a strong endorsement.

There are lots of interviews with Jon on Youtube, in various contexts. I’ve picked three – from three very different background environments – so you can get some feel for yourself.

2014 presentation – Jon Jayal at Amati, prior to becoming CEO

2020 interview – Jon Jayal with Proactive, just coming out of the worst of COVID

2022 interview – Jon Jayal & Johan Olivier with PI World, accompanying the last results release

Management also present regularly on Investor Meet Company, and, as always, reading the annual reports and seeing what is (and is not!) said is compulsory.

A case for bullishness

I’ve spent a lot of time on the past. I think there’s some truth in the famous line that ‘if you don’t know where you’ve come from, you don’t know where you’re going’.

But let’s now turn to the only thing that actually matters in valuation: where Quixant will be in one, three, and five years.

To put the ‘headline up front’, I’m targeting profits of $17.7m (£14.6m) in 2024. That compares to a current market cap of £97m, or a P/E ratio of around 6.6x. I should note that my targets are substantially ahead of broker forecasts for the company.

What drives my bullishness?

Firstly, market recovery. COVID battered Quixant’s end market in 2020, and it recovered only partially in 2021. There is a lot still to come at the very broadest level. Quixant’s 2021 annual report summed up the opportunity:

In short: there is 50% growth yet to come just to get back to pre-COVID run-rate levels of slot machine demand. It’s important to note that ‘pre-COVID demand’ was largely replacement of existing, tired slot machines. There was not an enormous amount of ‘new’ machine demand coming on stream (for instance, for new casinos in new jurisdictions).

Compare this relatively slow recovery in slot machine sales to the recovery in casino revenues. These have now set new records for the last 12 months. Casinos are taking more through their slots that they were before 2020. They are generating a huge amount of cash from their open properties, and welcoming many punters.

So there are two obvious tailwinds here. On the ‘necessity’ side, we’ve had 18 months of very restricted machine replacements – which one might hope leads to some catch up demand. And on the ‘discretion’ side, healthy profitability should loosen the pursestrings when it comes to casino capex decisions.

My second bullish driver is Quixant’s customer profile and new wins. On the latter point, I note that 2021 saw ten new customers enter production. I am sure these are of varying size. That said, I doubt it’s viable to run a slot machine business which doesn’t produce at least 100 units a year – perhaps much more. I have to assume that this will be a few thousand more in run-rate volume for Quixant. For context, they produced 40,000 platforms last year.

In terms of existing customers, we also have a nice little indicator, in that many of the major slot machine manufacturers are listed. This includes Everi, Quixant’s largest customer. This is gold dust for a curious researcher. If we can keep track of Everi’s volumes and outlook, we have a decent indicator of Quixant’s likely trajectory.

So what is Everi telling us? Well, hot off the press, we have their Q2 earnings call, where they said that:

“In the second quarter, our Games business sold a record 1957 gaming machines. For perspective, the last three quarters Games sales have been the best three quarters in our history…

… Supporting these cabinets is our growing library of innovative content in which we continue invest to ensure a robust pipeline of new original content. This enables us to support and maintain performance of our existing installed units and fuel further growth as we continue to march towards our latest target at 15% ship share.”

That all sounds pretty hot. And the outlook?

“With industry unit sales strong for the first half of the year, we expect to see continued strength over the second half of the year as operators remained comfortable with releasing additional capital for machine purchases.”

“… we said in our prepared remarks that we see a strong pipeline for unit sales in the second half of the year, team’s pretty confident in our ability to fulfill the demand that’s coming in for us in the current year as well. So we feel really good about that. Q3 started out strong for us.”

Everi’s shipments are now substantially above pre-pandemic levels. If they succeed in their target of getting a 15% ‘ship share’, they are looking at somewhere around 15,000 platforms. This compares to circa 5-7,000 annual sales pre-pandemic.

And – let’s not forget Ainsworth, Quixant’s old lynchpin customer. Recovery there is much slower than at Everi. They are a long way away from reaching their pre-pandemic heights. Still, market recovery is helping them along: platform sales in H1 2022 (which for them ended in December 2021) hit 2,718. If they hit 5,500 for the full year, that compares to 3,817 in the whole of the prior year and 3,634 in the year before.

Piece this all together – new customers, and clear and evidenced growth from existing key customers – and I think you have a great demand outlook.

Finally, on my bullish drivers, I point directly to the company’s commentary. In the group’s AGM statement in May, the company noted that ‘year-to-date’ order intake has been ‘significantly ahead of the same period in 2021 across both businesses’. Let’s look back to what they said last year. Are we comparing to a low base?

No – absolutely not. They said in 2021 that they had seen ‘exceptional order intake during the first half of the year’, which led to ‘115% order coverage of management revenue expectations’ for the full year, already at the half year point.

To be doing ‘significantly’ better than that sounds pretty good to me.

In the most recent statement, a few weeks ago in July, the group reiterated the strength of demand. They noted that ‘order intake during the period [was] ahead of first half revenues and prior year bookings’, which led them to increase both revenue and profit expectations.

A case for caution

Let me also address the two key risks I see in front of Quixant.

The first is supply chain. The semiconductor supply chain at the moment, to understate, is challenging. Over the las 18 months, Quixant have repeatedly pointed out the difficulty in getting shipments of necessary components and – if they can find supply- how much power distributors have over product pricing.

This situation is not new to anyone who invests; industries all around the world are affected, from automotives to home appliances.

But notions that it would be quickly abating seem to have been misfounded. I suspect Quixant couldn’t actually supply all the demand they had in 2021, and perhaps still can’t do so in 2022.

The global economy slowing down seems likely to take the heat off the situation – the supply/demand mismatch is getting smaller – but I do not think this is a ‘solved in 6 months’ phenomenon.

Additionally, talk of the economy worsening leads me to the second key risk: this is a economically sensitive industry.

I don’t know how Quixant performed in the last real downturn, but working from principles, we can assume they will struggle. Slot machines don’t have to be replaced in any given year. Operators can age their fleets. If casinos are struggling and footfall is down, capex budgets get cut. This will cascade through the system to harm Quixant.

If you are very bearish on the economy – even in the face of the gaming statistics I showed above – you will probably be more cautious on Quixant than I am.

For what it’s worth, I consider that there is something of a backlog of pent-up demand, which I think might mitigate some of the effects of any downturn that does come. I am also relieved that so much of Quixant’s business is tied to the US, which will have a much easier couple of years than Europe is set for.

Densitron

There’s another leg to the business which I haven’t touched on yet: Densitron. You might recall the name, as I mentioned it above. Densitron was the business many of the Quixant founders left when they went to do their own thing. It is an electronics manufacturer, providing displays to a whole range of industries.

In a scene straight out of corporate Hollywood, the apprentice swallowed the master: in 2015, Quixant bought Densitron.

I think the acquisition can best be described as ‘cheap compared to its potential’. Profitability post acquisition, to the extent you can analyse it (they consolidated legal entities in early 2020) does not seem especially impressive. Profitability before acquisition – as a listed company – was much the same.

What Densitron did provide the group, though, is the opportunity to expand Quixant’s horizons. The board knew this intimately; they had worked there, after all. Exposure to the broad customer base at Densitron provided the kernel which became the brilliant gaming business. Buying it gives them the opportunity to repeat that feat: direct relationships with customers, wider sales and engineering expertise, and a platform to try and grow a genuine ‘second leg’ to the group.

The area they have decided to focus on for the last five years is broadcast. Broadcast is an old-fashioned industry, with expensive technology solutions from decades past. Densitron have produced a range of modern hardware and software products which bring the media control room into the 21st Century: from modern button decks integrated into displays, to tactile control systems, to the software which sits at the heart of it, controlling devices. To be sure, they are playing only on the edges of an enormous market. But isn’t that the best place to start?

If I am honest, I have ignored Densitron for the last few years. Its contribution to the group is not great in profit terms, and disclosures by the company are pretty thin. It is hard to see what’s going on under the surface. It smells to me, though, like the great opportunity in broadcast might finally be coming to the fore. Densitron’s overall revenue grew by 21% in the first half of 2022, having grown strongly in 2021. The division finally seems to be breaking out from its historic ‘trading range’.

Broadcast is specifically called out, having grown 21% in 2021. It is repeatedly noted that broadcast margins are stronger than in the rest of the business. This is having a positive effect on divisional and group profitability.

If, like me, you like Quixant and have faith in their directors, you might see Densitron as having the potential to change the Quixant story: from a ‘gaming manufacturer’ to a ‘specialised engineering business’. This has the potential to drive a real change in stock market perception. I leave it to you to estimate whether you think this will happen.

Financials

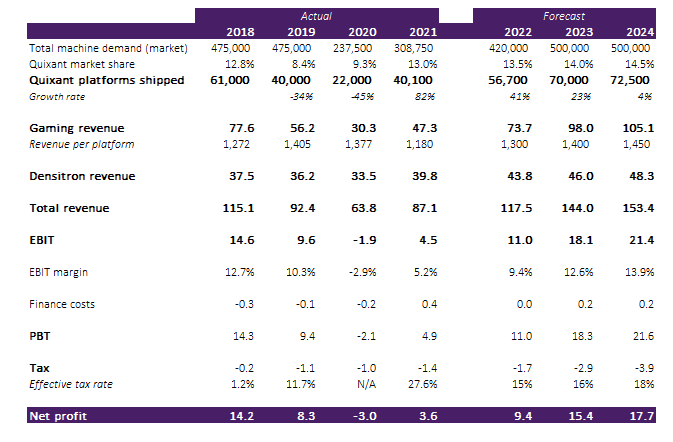

There’s lots of ways to try and model the financials. Here is one:

A few key things to note:

-

-

- My estimates for ‘total machine demand’ are similar to Quixant’s estimate of 475,000 – 500,000 machines annually. If you compare this to other sources on the internet, you will find very different figures. I think this is because of the different ways to define the size of the market. I have assumed a little bit of ‘catch up’ demand in 2023 and 2024, but not too much.

- I assume Quixant’s market share will continue to rise over the forecast period. I say this because of the strong growth at Everi, and because of the consistent customer wins they have seen. Prior to the last three years, this business had come from nowhere to double digit market share in its first decade.

- ‘Revenue per platform’ is a bit of a misleading number. It includes some peripheral revenues and has a wide mix of products. I wouldn’t read too much into it: but with inflation and increasing non-platform revenues, it’ll probably go up over time.

- I do not model Densitron separately. The disclosures on profitability have changed recently, and I don’t have a good steer for how much it’s really contributing to the group, or how well corporate costs are defined. One would expect historic Densitron to have a lower margin than the rest of the group.

- I also don’t try and disaggregate gross margin from EBIT margin here. Admin costs seems to move quite strongly with the revenue line, which suggests to me that there are a number of variable costs in the OpEx line. I don’t have a good enough sense of how these parts interplay. I do know that gross margins are massively suppressed at the moment, as the group has bought stock at inflated prices to ensure continuity of supply. When prices normalise, they will benefit. I also note that Quixant is a beneficiary of a strong dollar, noting the dollar has risen by 12% versus sterling year-to-date.

- The group’s tax rate will always be somewhat below statutory. They have a ream of patents, which allows them to enjoy patent box tax relief, and R&D spend is high, which also reduces the total tax load.

-

You can debate any and every point of this model. Indeed, if you are interested, I encourage you to do so. Let me know in the comments!

The final question is how this will translate to the share price. More than most businesses I look at, I think there is a very wide range of outcomes on this front. In 3 years time, we might be looking back and calling Quixant:

-

-

- An economically sensitive manufacturing business, never reaching its previous highs

- A high-quality gaming business, growing, but one-dimensional, or

- A diversifying specialised engineering business, attacking new verticals while growing its existing ones

-

One of the problems with investing is that current earnings performance drives price. Price then drives narrative. Which of these narratives prevails almost entirely depends on the earnings performance of the next few years. If the numbers go up, people start to think it’s the best thing since sliced bread. When the numbers go down, they suddenly decide it was a terrible business all along.

Here is how I see the world.

In the bear case, assuming we don’t have another COVID, Quixant might be worth around the current price or a little less. Their $120m market cap, minus $20m of excess cash, might be compared to $8-10m of sustainable net profits (substantially below the $14.2m peak in 2018), as a challenging market counteracts all their hard work integrating with existing customers and winning new ones.

I consider my forecasts to be the base case, though the brokers are much lower. Quixant might be worth around 15x earnings. Investors will look at them having grown profits significantly year after year, they will look at the historic exceptional performance of the business, and they will decide that perhaps there is a ’round 2′ of the Quixant story.

And in the bull case, people could get a lot more excited. As I mentioned, Quixant of years past traded at 30x earnings. Companies like DiscoverIE – which I consider to be inferior businesses – trade at 23x, even in the current market, as investors think there is runway for ongoing growth and acquistive expansion. I do think there will be a bit re-rating, though, if broadcast takes off. After all, if they’ve cracked gaming and they crack broadcast, what’s to stop them expanding further?

I’m not putting much stock in the final outcome. I like to leave the option value as option value until we get some more evidence the business can genuinely diversify.

But I do think my numbers are achievable, and I think it will drive a reassessment of the business. I target a share price of 330p in three years’ time, derived by taking my 2024 forecasts above, and multiplying by a somewhat arbitrary (they’re always arbitrary – don’t let anyone tell you otherwise) 15x P/E multiple. That multiple will always be volatile, in Quixant’s case, as investors swing from enthusiasm about the growth potential to concerns around the volatility. That’s investor psychology for you!

No-one knows or cares about Quixant. The bulletin boards are silent, the shares never trade, and most private investors have never heard of them. I think management like it that way. They are quietly executing. When the headwinds abate, I think investors will sit up and take notice.