Disclaimer: I have a material personal interest in S&U shares. A portfolio I help to manage has a large weight in S&U shares. Hence, I cannot help but be biased. Please do your own research.

Introduction

I want to pen some quick thoughts on S&U, as these are unsettled times for financial businesses.

While the current results show smooth sailing – something you can rely on with the family run firm – the underlying economic ground is moving faster than at any point in the last ten years. Inflation and fluctuating confidence both play their part, but I think interest rates are the most relevant variable. The core of any lending business is borrowing money and lending it out again. The structure of the way you charge interest and the way you borrow becomes crucial whenever there is a sharp movement in the rate curve.

Before I get to that, and by way of quick background, S&U is one of my largest positions. It is a brilliant business. If you want a long recap and to better understand why I think that, please read my two posts on S&U:

S&U Plc – Can’t get no love

S&U Plc – Credit where credit is due

If you can’t be bothered with all that text, consider that:

- S&U has grown earnings almost sequentially for the last two decades

- It is a family business. Enormous management ownership leads to the sort of stewardship culture which is uncommon in listed businesses

- Earnings quality is excellent. Profits are resilient. They have a defensible niche, and compared to peers their underwriting quality is superb

- Surprisingly for a financial business serving the non-prime end of the market, it has never lost money

- It is available for a little over book value, and circa 8.5x forward earnings. This is despite growing by over 10% a year and paying out a 6% dividend yield

With that out of the way, let’s discuss the pressing challenge the group faces today: interest rates.

S&U is a funny beast when it comes to interest rate impact. They finance themselves differently to most peers. I will use this post to consider the key risks and the obvious downsides of a higher interest rate environment. But I’ll also consider the potential opportunities – something I think many analysts and investors miss.

Finance Costs

Let’s start with the big and obvious negative: the direct profit impact of rate hikes. Unlike many lenders, S&U is not a bank. It does not have customer deposits. It primarily funds itself with shareholder equity, and a lot of it, as S&U is much less levered than its peers. But it also uses traditional bank funding lines.

The group has around £185m of debt, and though these facilities are various in nature, all are floating rate. Hence, every 1% increase in interest rate will increase their finance costs by ~£1.85m.

Some financial businesses have a natural offset to these rising finance costs, in that their lending is also floating rate. Many commercial lenders operate like this: they borrow money at SONIA plus X and lend money at SONIA plus Y. They ‘make a spread’. This makes them indifferent to the level of rates.

Some lenders use customer deposits, which are either non-interest-bearing or fixed for a certain period of time. These guys also have some protection from rising rates.

Alas, it is not so for S&U. Their borrowings are floating in nature. Their car loans and bridging loans have rates which are locked in at inception.

Hence, mechanically, rising interest rates will compress S&U’s net interest margin. They will pay more on their borrowings, and they will receive the same amount on their historic lending book. This will squeeze equity holders, who receive the residual benefit.

S&U is forecast to earn EBIT of ~£58m this year. Hence, each 100bps increase in interest rates will crimp earnings by around 3%. Not ideal, clearly. Not disastrous, either.

Impact on Customers

More important for S&U – and all lenders – is the state of the broader economy, and the impact that has on the quality of book debt. If you are lending on commercial property with high loan-to-values, for example, you start to get nervous when rates shoot upwards. What happens if the value of your security plummets? Will customers still repay their loans?

People fret about S&U in downturns because their Advantage Finance car loan subsidiary lends to non-prime customers. Cars are pretty good security. The threat of repossession is a strong incentive given most need their car to get to work. But the nature of Advantage’s customer base means that there are likely some historic issues around repayments on previous agreements. There might also be less of a cashflow buffer.

This is the extent of the analysis most people do when they analyse finance businesses. “In downturns, you don’t want to be in anything less than tip-top prime”. It is also completely wrong.

The truth is that it is very easy to cock up both prime and non-prime lending. All you can do as an outside investor is make a judgement on two things:

- Do I have enough historic data to validate that this business performs well through an economic cycle?

- Am I confident current lending is in line with historic lending, and hence the two situations are comparable?

Lending businesses are rightly proud of their scorecards, which assess which applicants should receive offers. It is very easy to grab outsized market share by being more aggressive with that scorecard. You relax a few innocuous criteria or become a bit less demanding, and your receivables swell.

As I mentioned in my first post on S&U, Advantage has not done that. They have two decades of excellent pedigree. They grew profits in 2008 and 2009.

Their highest ever impairment charge was 10% of net receivables, heading into the GFC. This is a large sum. They were further up the risk curve, then.

But it is not a particularly large sum when you consider they are earning a yield in the high 20s.

Ask yourself who you think is more likely to get into trouble. S&U has sufficient fat on its bones to withstand 10% annual additional debt write-offs and still remain profitable. Many of the specialist lenders, on the other hand, have thin interest margins and levered balance sheets. Some would turn unprofitable with between 1 and 2% of their book requiring impairment. Most have not been through a full credit cycle. Who knows where the skeletons are lurking?

Click: Why I’m not that concerned about consumer lending

To digress slightly: I have to say that I am much less concerned about consumer lending than many folks. It is possible to have worsening consumer sentiment, a poor environment for consumer discretionary stocks, and yet have healthy household balance sheets and strongly-performing lenders.

For me, the key difference is unemployment.

The current environment might be weak, but it is weak because we have high levels of inflation, high (but perhaps soon to be lower) levels of nominal GDP growth, and real wages not keeping up with cost pressures. This is denting consumer confidence. As a result, people are spending less on furniture, less on refurbishing their houses and less on drinking and eating out.

But, absent unemployment, you’ll find that people rationally realign their household budgets and do not stop paying for car loans or mortgages. They prioritise key payments. They will cut a cinema trip, trade down their groceries, stop eating out and defer doing up the kitchen before they stop paying for the car.

This sounds pretty obvious on paper: but I think it bears repeating that it is unemployment that presents the real challenge for consumer lenders.

You don’t have to believe me, either. We’ve had a ‘cost of living crisis’ here for 18 months now. Advantage Finance’s collections hit almost 94% last year and remained in that region as at the recent trading update. That is around the highest ever level.

Impact on Competition

So far, both impacts I’ve mentioned have been negative. Yet I’m relaxed about the impact of higher rates on S&U. I’m not delighted about them – but there are opportunities as well as challenges.

How can I square this contradiction?

It’s easier to see in the inverse: what is the worst possible relative environment for S&U?

Firstly, it’d be an environment with a very low cost of debt capital. S&U funds itself with vastly more equity than a typical lending business. Lenders who are only looking at the marginal cost of an incremental pound have been very aggressive in the last five years. They have taken advantage of cheap debt to throw money out of the door by being more competitive with rates. They have jacked up the cost of customer acquisition through intermediaries, as there is more capital competing for a stable pool of deals.

And secondly, it would be a period with very predictable and stable economic conditions. As I mentioned before, it is easy to grab volume in a lending business by being more lax with your lending criteria. If times continue to be good and unemployment continues to be low, you likely won’t be found out. But your marginal lending – the customers you probably shouldn’t have taken – are the ones which will hurt you most when the economic cycle turns. If that economic cycle never turns, there is little ‘pay-off’ for prudent lending behaviour.

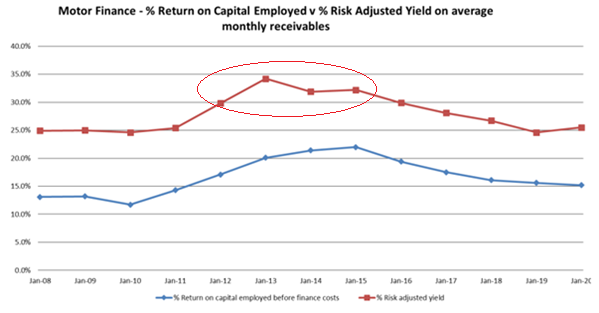

In short, you need some stress to actually forge good long-term returns in financial businesses. As I have mentioned before, it is no coincidence that Advantage’s best ever period was the years immediately following the financial crisis. Consider the chart below:

Advantage was finding prime customers at non-prime rates. Finance had dried up. No-one was lending. Being a well-capitalised survivor allowed you to pick and choose from high quality credits and name your price whilst doing so.

Summary

I know what I’d be thinking if I read this post: it all sounds a little too convenient. I’m trying to spin an obvious headwind as a tailwind. It’s like saying car manufacturers should be happy in a deep recession. It doesn’t make any sense.

I recently met one of the executives of another listed business facing real challenges at the moment who told me:

“At this point I just want to see the world burn: interest rates as high as possible, steep recession, whatever. Because I know that if it’s challenging for us, it’ll kill everyone else. We are the most competitive, and we will survive, and it’ll be a lot easier on the other side”

That resonated with me.

Investors should have a nuanced view toward the economic cycle. The value of a firm is not captured by simply taking a multiple of next year’s earnings: and there are situations and events which can have a negative impact on that earnings figure but which are accretive to long term value.

This is all highly dependent on the specific competitive environment for the company in question. I own businesses where I would not be making a case like I am here: businesses which are not the market leaders, with structurally advantaged economics.

Often, I would rather an easy ride. There are lots of ways of investing, and I am not tied to only investing in ‘the highest quality businesses’ or solely ‘market leaders’. Investing is full of rules and exceptions to rules.

But for S&U, I’m sitting here and wondering what I am wishing for. Do I want a smooth recovery, such that Advantage can continue gliding along as it has done so excellently for the last few years? Or might we be better served as investors if interest rates keep rising, stresses build up, and the competition – none of which is close to as high quality or well finance as Advantage – have to blink first?

It’s a tough call.