Disclaimer: I have a very material personal interest in S&U Plc shares. A portfolio I help to manage has a very large weight in S&U Plc shares. Hence, I cannot help but be biased. Please do your own research – my projections are mine alone.

Elevator Pitch

I’m a firm believer that, if your stock idea is a solid one, you should be able to explain it in one minute. No bells and whistles, no complications. So here goes:

S&U is a financial holding company with two divisions. The dominant one is Advantage Finance, which lends money to car-buyers with imperfect credit histories.

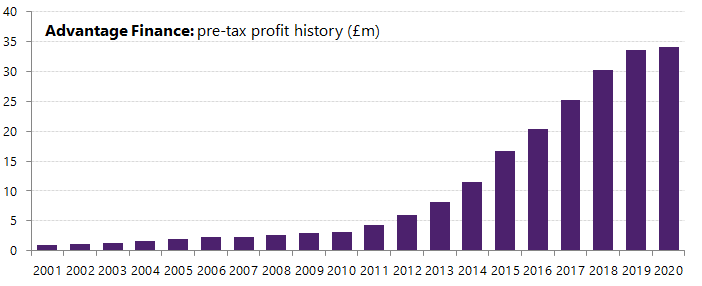

This is an inefficient and hands-on market: you have to actually price for risk and be selective with borrowers. But it’s also very lucrative: since foundation in 1999, Advantage has grown profits every year at a 20%+ clip. Return on capital over the last decade is consistently 16-17%.

Management and their families own half of the outstanding shares, and you can tell from the way S&U is run. The company is fair to its customers in a space where many are not, and the balance sheet is conservative. Their 18% annual total shareholder return over the last two decades is not built on leverage, but on underwriting quality. And – no surprise – they reward shareholders with large dividends, even while the group is growing.

You get all of this at a 7.3x historic P/E, or a smidge over net asset value. This year will be tough – earnings will halve, driven by big, one-off provisions – but the group is then set to rebound and carry on its prior trajectory.

My assessment is that business growth and dividends will drive a 13%+ annual return for investors here, even if S&U were to stay at their current miserly multiple. Those are the investments I love: companies which are fundamentally creating value every year and are cheap to boot.

And why is it cheap? Simple, I think: no broker covers it with any attention, it’s too illiquid for most institutions, and most private investors (rightly) shy away from financials. S&U gets lumped in with the rest, when it’s a diamond in the rough.

Yeah, yeah, I know what you’re thinking. “You must be a bloody fast talker to fit that into a minute”. Luckily, I am.

Advantage Finance

Let’s go into a little more detail on the key division I mentioned above – Advantage Finance.

Advantage Finance is a provider of non-prime, hire purchase car finance: they help people with imperfect credit records buy used cars. They lend around £6,500 on a typical deal for about 4 years. The customer makes a fixed monthly payment and ends up owning the car.

If you’re already dragging your cursor up to the top right of the screen to close the window, give me a little more time. I also hate investing in financials: they’re opaque black boxes. Trust me when I say – like you told your first girlfriend – that S&U is not like the other guys.

Here is why it’s worth giving them at least a couple of minutes:

In any other sector, S&U would be lauded as the success story it is, and investors would be pontificating about growth runways and how high the multiple should be. Because it is a financial, they are not: they lump it in with the banks (inefficient and bureaucratic) or the spivs and chancers (profitable, until they spectacularly blow up).

But Advantage is neither. It is better: it is differentiated, hard to replicate and surprisingly resilient. Why?

Most obviously, it is because non-prime credit is meaningfully less competitive than the prime space. You cannot fight the banks. Banks are lending machines, with incredibly low funding costs and a business model predicated on maximising both assets and leverage. That is not the game Advantage plays. Advantage is a business built, from the ground up, on good underwriting. Just as we stock pickers are looking for misunderstood and mispriced companies, Advantage is looking for mispriced creditor groups.

And it can do that because, when you leave prime behind, the competition thins out rapidly. Lending where you have to (shock horror) underwrite some risk of non-payment, which can’t be captured by a broad macroeconomic overlay, is hard. You need data. You need twenty years of track record lending to self-employed van drivers in Hull who’ve had a CCJ, and you need to be able to appraise their current income and their propensity to pay.

The upside of doing that work is that you make actual returns. Advantage is currently charging, on average, a flat 17% interest rate on lending. It’s true that a small proportion of Advantage’s customers can’t pay or require some help. But the risk-adjusted yield – a measure of the revenue minus the required impairments, in cases where you don’t get your money back – is still excellent. Advantage’s underwriting ensures that they are getting paid for the risk they take:

Let me address the ethical elephant in the room early: yes, this is non-prime credit, and yes, the interest rates are high. They are not payday lending high, but they are high. And as you are reading an investment blog, statistically speaking, you are probably rather comfortably off, and you probably feel your eyes twitching at those double-digits. You can likely borrow at 3% APRs, not 28%.

I think Advantage Finance provides a good service lending to people who otherwise could not get finance, and they price appropriately for the significantly increased risk they are taking. If you’re on the fence, I’ve included a bit more on the ethics of Advantage Finance in the accordion text below.

The ethics of non-prime lending

Lending to non-prime customers means accepting that in a moderate proportion of cases you will not get your money back. You have to price for this risk. You also have to price for the work you do to acquire, segregate and analyse the huge wave of loans: Advantage write policies on less than 2% of their applications.

All of this adds cost. There is only one alternative to pricing for risk: and that is to not lend to individuals with imperfect credit histories, deeming them unworthy of credit on the very asset they could use to improve their earnings prospects. Personally, I find that to be a pretty extreme point of view, although I acknowledge it is a view some people hold.

If you do agree with me that people should at least have the opportunity to access credit, the question then becomes who is providing it and how it is provided.

The rules on lending in the UK are actually pretty good, and very consumer-friendly. Take, for example, the requirement for affordability. It is up to the lender to complete ‘reasonable and proportionate checks’ to make sure that borrowers have the capacity to repay loans. The onus is placed with the lender. I have seen cases of ‘unaffordable lending’ alleged where the lender did not check bank statements: which apparently they should have done, because they would then have seen gambling charges which the customer did not previously mention in their self-reported affordability calculations. I have read cases where lending was deemed unaffordable because Advantage were being too aggressive in assuming the other earner in a household would contribute to household bills; Advantage apparently, should have assumed that the partner was freeloading and that the applicant would pay for all rent, food and utilities on their own.

That said – I am not naive. I am under no illusion that the non-prime credit space is squeaky clean. Unsavoury characters can be attracted to high interest rates, and there are a greater proportion of vulnerable customers in this segment of the market. The rules are good: the interpretation and application of those rules are often not.

If we further consider the usual incentive structures of financial companies, it’s obvious how problems arise. Take the pay-day loan business: large fixed cost structures and huge marketing expenditures, but each loan is incredibly profitable, at triple-digit interest rates. Customer acquisition is very expensive. To where does this lead the business model? Unsurprisingly, a ‘lend at all costs’ strategy, with a high proportion of re-lending to inappropriate customers.

Advantage Finance is not like that. It is not private equity backed, with a growth-at-all-costs mentality. It is family owned and sensibly run. It slows down lending when it is uncertain about the environment and about affordability – like now, for instance, when credit reference data is essentially useless given payment holiday distortions.

The way I became comfortable with the culture at Advantage is by reading all of the Financial Ombusdman case decisions on the company back to 2017. There are hundreds of these online. The Financial Ombudsman is an independent regulator, used by consumers when they feel they are being unfairly treated by a financial services company. Cases which make it through levels of arbitration are posted online. You can read them and you can assess for yourself whether Advantage is a company which treats its customers honourably and fairly, or whether you think they are trying to screw them at all cost. My answer, in this case, is empthatic: Advantage does the right thing. It is not perfect – no-one is – but the culture is strong. I expected to find a handful of instances where Advantage had clearly stepped out of line or dramatically mishandled things. I found none.

Prior to COVID, Advantage was growing nicely. Reported financials lag underlying business growth because new borrowers in a year only meaningfully contribute to profitability and revenue in the next year. So although 2020 was a slow-growth year from an accounting perspective, that actually reflected the caution in the prior year, which saw the group contract lending quite meaningfully in the face of tougher competition and worsening loan quality.

That trend reversed in 2020, and coming into the crisis we hence had good visibility on future growth: receivables (money lent to customers) at year-end January 2020 were up from £259m to £281m and advances (new money lent) were up 15% year-on-year. In other words: 2021 was shaping up to be another solid year in a track record full of solid years.

Aspen Bridging

Aspen Bridging is S&U’s internally founded new division, writing property bridging loans. I will keep this section fairly brief, as Aspen is not currently hugely relevant to the valuation of S&U. Receivables are around £20m (less than a tenth of Advantage), profitability is a single-digit percentage of the group’s total, and growth in the last two years has been slower than I had expected.

Rates are from 59-89bps a month, in addition to the usual entry/exit/variation fees which beef up returns. Allowing for a bit of loss (defaults should be low, and loss given default should be minimal, barring fraud) I expect this is a 10-12% return on capital business in the medium term, with lower returns than the car finance business being somewhat ameliorated by better security and the much bigger size of the addressable market.

While certainly better than the bank mortgage business, I do get the sense that bridging is becoming increasingly competitive. I view it as less differentiated than car finance, and I also think it’s trickier to carve out a real niche in a segment with residential security. The beauty of the car finance business is that it is not far from unsecured lending – the loans are undercollateralised, not overcollateralised – which gives you, as a lender, a lot of scope to add value if you can correctly appraise customer propensity and ability to pay. Bridging is not like that. Everyone uses similar valuation reports to value the same four walls. The question is how aggressive you’re willing to be to get the deal, or how you can add value through speed and relationships.

All of that said, I’m happy to be proven wrong. S&U give off noises about trying to scale this bit of the business quite quickly, and I suspect the current size is substantially below where they want it to be: a real ‘second pillar’ of the business would require an order of magnitude more lending than they’re at currently.

What it does highlight, though, is the group’s entrepreneurialism. The group decided it need another leg to stand on, looked at hundreds of acquisitions, found none priced at levels at which they wanted to transact, and so started a business from scratch. I think investors very often overlook what decisions like this say about businesses and management teams. Boards nearly always choose to buy, not build. Building is hard work and takes time. Buying is immediate: immediately exciting, immediately accretive. The trade-off, of course, is that you shell out a premium to do it; you pay someone else to sweat for eight years of their life to build a business so you can be impatient.

You can divine a lot about management’s attitude toward shareholders, and their stewardship of company capital, from decisions like this. S&U’s management treat their capital as a precious and scarce resource. That attitude permeates an organisation.

COVID Impact

Call me crazy: but I think that, despite the share price fall, COVID may actually be a positive in the long-term for S&U as a business. Or, at the very least, that the obvious negativity has three silver linings which mitigate much of the damage. In order of importance in my mind, I see:

- Better long term risk-adjusted yields: tough economic environments scare capital out of the non-prime sector, boosting returns for the survivors

- Cost reduction: S&U has taken a good deal of cost out, particularly in loan acquisition and underwriting (not, importantly, staff)

- Better investor perception: capital markets will get a fresh reminder of how different S&U is from its ‘peers’, as they will trade profitability through calendar 2020

But before I wheel you off into the sunlit uplands, let’s deal with the very real negatives. S&U lends money to non-prime customers. Non-prime customers – and the clue is in the name here – are more likely to struggle in tough economic environments. Ergo, COVID and the associated impact must be terrible for S&U. Right?

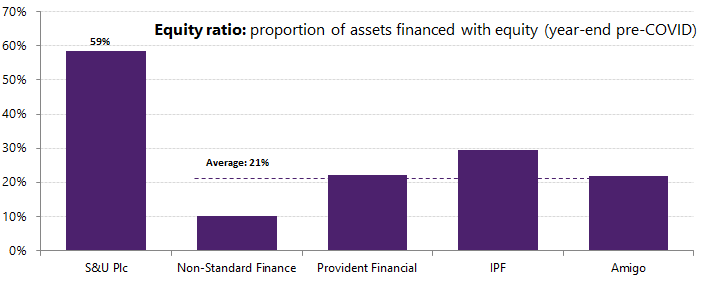

Point one in the defence of S&U, which I mentioned in the preamble, is the financing structure. S&U is exceptionally conservative compared to most financial companies. The below chart shows the equity ratio for S&U and a selection of non-prime lending peers. In essence, it shows how much of the lending a group does is backed by shareholder equity instead of bank loans.

You will note that for S&U, every £5 of lending is supported by ~£3 of book equity: they lend mostly their own money, with a little external funding to improve shareholder returns.

For most peers – and Provident Financial is probably the best comp – £5 of lending is supported by ~£1 of book equity.

It is hard to overstate how important I think this is from a long-term stability perspective. Non-Standard Finance, which you see in the chart, came into the crisis with the most levered position. They come out of the crisis likely to breach their banking covenants, with going concern status propped up by ‘the assumption of lender and shareholder support’.

S&U comes out of the crisis having paid off some of their bank debt, never having furloughed any staff and still paying a (modestly reduced) dividend. The difference is stark. That S&U makes a far better RoE than its sector, despite much lower leverage, is testament to how good underwriting quality is.

Point two in the defence of S&U is the group’s excellent performance in the last financial crisis. In 2008 and 2009, the group grew profits both years. They will not manage that this time – the FCA’s hamfisted approach to payment holidays and the extreme levels of uncertainty around the economy in 2021 necessitate conservative provisioning – but that GFC performance served as an important bedrock for me when I was buying in March and April, when the world seemed a scary place indeed.

Fundamentally, we have to consider that in a typical year the group is earning a 25% risk-adjusted yield, and impairing 6-7% of its loan book. In 2009/10/11 that impairment reached 11%. But when you are making a 25% risk-adjusted yield, you have a lot of slack. Impairments can double and your position is still sound and profitable. Typical investor heuristics about how quickly financial companies blow up just don’t apply here: this is not a bank lending at 2.2%, where a 3% impairment rate destroys the business.

So in terms of immediate solvency risks, the first thing people panic about with respect to lenders, I see essentially none. Further, I believe we have already seen most of the impact of COVID in S&U’s financials. The half-year reported a very large additional impairment to account for uncertainty around coronavirus: the company has ‘taken its medicine’ and written loans down in advance of actual defaults. I suspect H2 results will see the group prudently putting a little more aside in impairment.

The slowdown in lending through lockdown is perhaps the bigger medium-term ‘damage’ from COVID. Payment holidays, the irrelevance of credit reference records and the economic uncertainty have all conspired to see Advantage reduce lending significantly in the first half of this year. The group’s previous glide path to £40m of net profit is hence set back a couple of years: less lending means lower future profits.

Those are the negatives, and they are real. But let’s be honest: in the grand scheme of things, these are not earth-shattering problems. Modestly less profit on the existing loan book, to allow struggling customers extra time and to write off what is necessary, and a slower growth rate in 2020 and likely 2021. When we have a significant proportion of corporates losing money in 2020 or having to raise money in the middle of a market sell-off – something a surprising number of ‘stable’ companies did – S&U’s woes seem eminently manageable in comparison.

As to the key positive?

Well, if we look back ten years, I note that the post-GFC period saw the best loans that Advantage Finance has ever written. Scroll up to the ‘risk-adjusted yield’ chart above and you will see levels pushing 30%. Why? Because crises make lenders retrench. Most companies are not financed like S&U, and do not have the institutional setup to zig when others zag. They see distress in the market and stop lending to any customers except the very most creditworthy. That pushes otherwise good business to the hands of S&U, who are able to lend at good rates to customers who will experience extremely low default rates.

I don’t think Coronavirus will lead to the sort of incredible returns we saw in 2013 and 2014 – I don’t get the sense that capital has withdrawn to the same extent as it did then – but this mechanism is worth bearing in mind. And, just to whet our appetite, in S&U’s latest investor presentation we got the tiniest taste of a movement in this direction:

The chart is hard to read if you have not seen it before, but it is interesting. The blue line shows the proportion of customers who make their first payment on time – a simple measure, but an instructive one, because you will note that is correlates quite strongly with the red line – which shows the ultimate loss ratio on a cohort of customers. The observation is thus that if a cohort of customers mostly makes its first payment, it is likely to have a lower observed loss ratio for the full loan term.

The dotted red line is the area of uncertainty – because these are loan cohorts which have not concluded yet, we do not know the ultimate loss ratio.

Tantalisingly, you will note that the loans the group underwrote in May and June have first payment performance not seen since the post-GFC days. I am cautious about the continuation of this trend, but if we see first payment percentages staying at anything like this level, we have a very positive indicator for the future health of the book indeed. We may not be ‘getting back to pre-COVID levels’, we may be significantly exceeding them.

Management

It is hard to write about management, because views on management are inherently subjective. To stay rooted in fact for a moment, I note that:

- The management team currently in place are exceptionally long-tenured. The Coombs brothers (Chairman and Deputy Chairman) have been leading the business in various forms for 45 years, while Chris Redford (Finance Director) has been in the group for two decades. Only Graham Wheeler (CEO of Advantage Finance) is a fresh face, following the retirement of the previous MD after two decades on the job.

- They have overseen a superb, multi-decade track record of double-digit shareholder value creation

- They and their families own around half of the company between them

That, in itself, is a good starting place.

More important to me, though, is my assessment that they are fundamentally good people. It is always hard for investors to acknowledge that one of the most important parts of an investment thesis is as woolly as this – a judgement on management competence and integrity – but there is no getting around it. If you are investing for the long-term, you are backing a management team, and you need to be very sure they are taking care of your money.

Their honesty and competence is not something I can persuade you of, so I won’t try. Instead – if you are interested – I invite you to read everything you can. S&U has annual and interim reports stretching back to 1999 online. Anthony Coombs, the chairman, also does a good job of trying to update the market through alternative channels – you can find a bunch of interviews with him on Youtube. I like this fairly recent one with Graham Neary:

There is also a recent results presentation on InvestorMeetCompany, if you want a more fulsome discussion of the business, as well as a chance to see the wider management team present.

You will discover, if you do dig through enough interviews with Anthony, that his line never changes. He starts nearly every interview by talking about the ‘identity of interest’ between management and outside shareholders, given their common objective in improving returns. ‘Steady and sustainable growth’ is a phrase I half-suspect Anthony has embroidered into his lapel. (I originally wrote ‘tattooed on his arm’, but considering Mr. Coombs is an ex-Tory MP of the old school variety, my wager is on the embroidery)

I love this. This is a management team with an unfailing focus on shareholder returns by doing the right thing for the long term.

Financials

I have thus far tried to lay out why I think that:

- S&U is an excellent business to own for the long-term

- COVID-19 is a blip in the long-term history of the group, not a structural challenge. In fact, it may prove to be mildly helpful in coming years

- Management are honest, straightforward, and aligned with us as outside shareholders

What should one pay for all of these characteristics?

I know what I think is the wrong price: and that’s £17.60, or a little over tangible book value, or 7.3x earnings.

I tossed and turned over how to present this section because there is no getting away from the fact that financial accounting is complicated and subjective. Revenue is not, as one might assume, the interest received in an accounting period: it is instead the output of a spreadsheet amortising a loan balance down and trying to keep a constant return on capital based on the assumed IRR of that loan. Receivables are stated after provisions which are entirely a product of assumptions about future macroeconomic indicators and default rates.

This means you have to trust management and believe they are on your side.

But it also makes forecasting difficult, if not impossible. To forecast the profit number for this year, I need to read the collective mind of the management team. What do they think unemployment will be? How conservative will they be in making provisions for customers who have not defaulted but may do so in the future?

If you are smarter than me – and have a good way of forecasting results at companies like this – please get in touch. I would love to compare notes and try to think about a framework. I have a few different models for trying to estimate revenue in cohorts, and a simple ‘cash accounting’ approach to the Advantage business which is instructive but hard to translate back to financials. I am also always trying to figure out what I can read from the tea leaves of the provisioning numbers.

But to simplify down to its very basics, we can boil S&U down to a few variables:

- How big will Advantage’s loan book be in three years’ time?

- What will the risk-adjusted yield be on that loan book?

- How big will Aspen Bridging’s loan book be in three years’ time?

- What will the risk-adjusted yield be on that loan book?

- How much will the company have to pay to acquire those loans (to brokers and intermediaries)?

- How much central cost will the group have?

- How much interest will the group pay?

And if we spin up an ultra-simple model with those assumptions (I’ve hidden a few calculation cells below to keep it light, but you will get the general gist):

… we see a group which can make £34.4m in a few years’ time with realistic assumptions about the pace of lending and the profitability of that lending. Note that I have given the group no credit for an improvement in risk-adjusted yield (so no ‘improving market’, despite early indications) and only assume that, by 2024, Advantage’s loan balances are ~19% above their prior peak. This business was growing at that rate in a single year not long prior to COVID.

I am assuming fairly rapid growth at Aspen Bridging based on their public pronouncements, which suggest their deal pace accelerated quite rapidly around the middle of this year. I also know management want this to be a much larger part of the group, so I suspect they will be very keen to drive growth. That said, it does not change the model that much if we slow down growth there: I am only assuming a 10% risk-adjusted yield versus a 4% cost of debt funding, so the differential is not enormous.

My bet is that the group will get to around that £34.4m net profit number in 2024, and once the COVID-smoke clears, the group will be back to trading on the 12x earnings multiple – equal to a slightly sub-2x tangible book multiple – on which it has spent a decent chunk of the last decade.

That equates to £34 a share, sometime in 2023 or 2024 depending on how forward-looking the market is at that time. In the meantime, the group will pay you a healthy 6-7% dividend yield.

Frankly, I still find this a very low multiple for a business of S&U’s quality. How many other companies have the track record here, with such evident management quality? I struggle to find them. I would happily pay 12x for a business of S&U’s pedigree. I am fortunate that the market is not asking it.

Ultimately, the valuation here is your margin of safety on expected returns. At the current valuation, if S&U never grow their loan book again investors are still looking at a 12%+ RoI investment without any multiple expansion. Hell, if S&U were forcibly told never to lend money again – and simply run down their existing loan book – you still make money at the current price. That is how much cash this group throws off. And with a management team of this quality – with this much of their own money invested – it is never likely to be a value trap. If they cannot profitability invest, they will not squander the money on vanity projects. They will give it back, as they have been doing for decades.

S&U has been left behind in the vaccine rally. It is one of those forgotten stalwarts in the dusty corners of the small cap market, with a couple of posts a month on the bulletin boards and very little sell-side coverage.

And all of this is why I have so much money alongside the folks at S&U Plc. It is not riskless – no investment ever is. There is always the chance that controls are breached or something goes catastrophically wrong: that’s investing. But I am sitting alongside two individuals with a lot more to lose than me, and the risks which are in their control seem to be managed very well indeed. The company is ethical, soundly financed and ably managed. I suspect that, sooner or later, the market will see these virtues, too.

Great write up thanks. What do you think of FCA intervention? Given they’ve been hot on sub prime lending of late (e.g Provident/Amigo etc). Although arguably that could be due to lax lending requirements.

Thanks JS:

S&U came out clean from the last FCA look into motor finance, which looked at variable commissions – commissions which vary based on the interest rate ultimately paid by the borrower. Obviously, such commissions incentivise brokers to screw their customers. Advantage never used any of these. (one tick for the company)

As I mention in the section on ‘ethics’, I also spent a lot of time looking at the Financial Ombudsman cases in which Advantage have been involved. While it’s far from a robust regulatory look at the business, it gave me some confidence that the culture is strong. There wasn’t a single case where Advantage had done anything which made me wince or made we worry about intervention. The vast, vast majority of cases involve a faulty car – which the customer says was faulty at the point of purchase, and which Advantage says broke after that point. In other words: not really Advantage’s fault, although they are obviously on the hook as finance provider.

The FCA is getting increasingly heavy with sub prime lending, so I do think it is a risk, although it is potentially an opportunity as well. Barring anything crazy like interest caps I struggle to see what they could do which would damage Advantage more than the competition.

Do you have a specific concern? Would be interested to hear if there’s something I’m overlooking.

Hi Lewis! Sent you an email, but it may have gone to Spam. In the email I attached the FOS/FCA complaints, which it sounds like you’ve already analysed!

In short you’re right. Unlike Amigo where it was clear of rising FCA complaints/FOS before the market caught up, Advantage Finances FCA and FOS complaints are stable.

Amateur question, but the interest rate you quote of 17% is substantially lower than the revenue/Avg. receivable book? Is there a bunch of additional costs for customers/or is that on gross lending or just a misunderstanding on my behalf?

Hi JS,

Can’t find it in the spam either! Could you try again to lsr@lewissrobinson.com? Appreciate it.

Re: the interest rates: no, that’s a very good question. There are some extra costs – arrangement fees, commissions from GAP insurance, etc. etc.

But the real answer is that I and they are referring to a flat 17% interest rate, which equates to a substantially higher APR. I.e., if your loan is £5,000, you pay £850 every year, even as your loan amortises down. If you dig through the notes of the annual report each year, you’ll find the effective interest rate of their book of loans… last year it said:

“The average effective interest rate on financial assets of the Group at 31 January 2020 was estimated to be 28% (2019: 28%). ”

Let me know if I have explained that poorly.

fantastic, we would like to read you more, great job, thanks for sharing time and knowledge, it would be a pleasure to be able to subscribe to receive more content, but I don’t see it, greetings

Hi Nicolas,

Thank you for the kind words. There is now a subscribe button (at least if you are on desktop/laptop!)

Best,

Lewis

sorry, I don’t see this button, I tried in chrome and firefox and I couldn’t find it

Great writeup. Thanks. You asked for potential concerns so here are a couple…

What do you make of the atrocious grammar and nonsensical statements in the 2020 Annual Report (particularly the middle section)? Is this sloppiness evidence of a deeper malaise?

Is the of hiring an external big hitter as CEO of Advantage sensible when they make a big thing about family values and staff loyalty etc. I believe Advantage is run from Grimsby but head office is in Solihull so keeping an eye on the new boy may not be straightforward and if nothing needs changing why pay up for a potentially large ego?

Hi Nero.

Excellent! Thank you for the thought-provoking points. Both of them are interesting.

Re: the attention to detail in the annual report:

I would say that ‘atrocious’ grammar is a little harsh, although more proofreading would certainly not have gone amiss. It’s hardly an auspicious start when on the first main page they say:

“We are key members of the Finance and Leasing Association (FLA) who help shape the industry, help shape the industry.”

As to whether sloppier annual reports correlate with sloppier execution in other respects, I’m really not sure. It’s an interesting idea. Broadly, I would say that the report gets across all the points it needs to, so I’m not too offended by the stumbles. It may simply suggest an annual report which had less expensive external involvement, which I would view as a rather good thing. In an ideal world, of course, we have a polished report with eagle-eyed board members picking up these things.

Re: the external appointment at Advantage:

There, actually, I have to disagree. I don’t necessarily think staff loyalty and family ethos necessitate an internal appointment. I generally think that after 20 years of management by one CEO and his appointees, the injection of some fresh faces is a good thing for any business. I note that Graham Wheeler seems to have the bit between his teeth on a number of new affinity channels for the business – new ways of generating leads – and is digitising Advantage so that customers have phone and online portals. The latter, one might argue, is a sign that some ‘freshening’ was needed.

Having said that, to be clear, I was disappointed when Guy Thompson stepped down. It would be crazy to suggest that one would ever be happy when the CEO who founded a business and led it through 20 years of double digit profit growth resigned.

The recruitment process for Graham was quite long and there was a lengthy handover with Guy. His credentials also speak for themselves. I think it was a good appointment, noting all of the risks you mention (and your Solihull/Grimsby one is definitely one I think about).

Again – thank you. I am always a little hesitant about counter-arguing to criticism as I don’t want to come across as if I am trying to bat away or argue down the negatives. Your points are well made and I appreciate you making them.

Best,

Lewis

Hi Lewis

Thanks for taking the time to write this. It made for an intriguing read and certainly worthy of being added to the watch list.

One thought if I may.

Given that it is likely that:

a) 2021 will be a recovery year,

b) the full dividend will resume in 2022,

c) any share price recovery doesn’t “appear” imminent

might it not make more sense to buy mid-2021?

Aside from having some more re-assurance around all things covid, the opportunity cost in not investing in larger recovery plays right now seems quite large.

Would you agree? Or would you be hoping for a much quicker recovery in the share price over the next 6 months?

I do actually believe in being able to “time the market/a share” to some extent, so given the lack of equity research and high management ownership any risk of it being taken over in a lowball offer, or materially re-rated seems low right now.

Unless I’m missing something blindingly obvious.

Cheers again

Abs

Hi Abs,

Thank you for reading, and glad you enjoyed it.

I agree with all of your points of reflection. I suppose the question is the extent to which one feels comfortable and confident timing the market, as well as the perceived opportunity cost if one gets it wrong.

To my mind, I think S&U offers a mid-teen annualised return through to the medium term, even without any multiple expansion. I also think it does that with very low risk of capital impairment (management alignment + the fact the book is worth more than current trading price in run-off mode). If the multiple does expand within the next three years as I expect, it’s a 25-40% IRR.

I could try and do better, as you point out, trying to match my trade with the more likely timing of a recovery. But at what cost? If I can get comfortable that it is a mid-teen IRR opportunity with conservative assumptions, I would be passing on that solid, above-market return for the hope of more. And if the market, in 3 months, decides it does want to be forward-looking with S&U – as it is with so many other stocks, looking ahead a few years to ‘normalised’ earnings, I will miss the gains. In that scenario, my portfolio is much the worse for it. S&U is an illiquid stock with poor coverage and little investor knowledge. I don’t think it takes many positive trading updates, or a few research notes from brokers, to get it moving again.

It is, I think, simply an expected value analysis – like all portfolio management, I guess. How strongly do you rate your own skills in timing the market? What are your other opportunities for deploying your capital in the interim? I am not confident on the former and do not see so many stocks where I am confident of a mid-teens return with minimal downside. That explains my positioning.

As to other recovery plays – by all means, please let me know! Love hearing about people’s positions!

Best,

Lewis

Genuinely enjoyed reading this and prompted a lot of thoughts regarding my holding in PCF, where there are many parallels. Though PCF is attempting to move closer to prime & has a slightly different lending suite & of course is now a bank.

I agree on the bridging finance angle where PCF are also at a similar stage in their development. In, short it is a competitive market and I think they are all starting to look like they are chasing the market. However, rates are also high and forgiving with a secure process in the event of default. I think I read somewhere that there is structural growth f/c, so perhaps they all see what we don’t see in this mkt, which could be good collateralisation, high recovery and generally appealing rates vs funding costs.

I too have tried without success in figuring out how do f/c impairments. I’ve also quizzed the CEO on it and am still not sure I see anyway of getting ‘inside’ the model & its clear no one wants to disclose anything they don’t have to on it.

I like your model and think it makes sense, though a tough 21 is the real risk here & in my view explains the low valuation along with the other material factors you point out.

Before I looked at your valuation, I did a very quick and dirty one using BV and came up with: I think it could return to a p/bv (my preferred measure vs P/E) of at least 2.0x in a more forgiving mkt & without working through any maths if BV can appreciate to £16-£17 per share vs c£14.35 in the coming 3 years, which based on historic growth looks a rational bet, that makes it £32-34 per share at some point in the coming 3 years.

Look forward to reading the next one.

All the best.

Paul

Hi Paul,

Absolutely no insight on PCF, so I won’t write any words on that as I’d be out on a limb. But thank you for the thoughts: I do need to look at the banks in more detail. PAG, PCF and STB all look ostensibly cheap.

Re: tough calendar 21 (which is their ‘2022’) – a key risk, I agree. From an existing credit perspective I’m quite relaxed given the high level of provisions I’m assuming they put in this year, and I’m assuming they also have to put another 2% of receivables aside next year on top of the prior ‘norm’. If they have to put another 5% on top of that again, the impact is another £13m off net profit – annoying but not destructive, assuming it is a one-off hit. From a lending volume perspective, I’m less certain, and I also think that’s a bigger risk for the long term equity story. If lending growth doesn’t resume, earnings growth won’t resume, and the rating will struggle to return to prior levels. To keep the RoE at levels which justify a 2x book value, they will need to put their foot back on the gas in lending terms in calendar 2021. I hope my assumptions are conservative, knowing management and knowing their desire to restart lending, but I am certainly out on a limb on this.

I know financial types like P/BV based valuations and I’m with you on the broad strokes: think an 8% cost of equity is broadly about right, a 16% return on equity is achievable based on historic levels, and hence 2x P/BV is probably a reasonable target. It’s traded around that level in past, prior to the consistent de-rating of the last couple of years. As you point out, we then end up roughly the same place in terms of valuation level, with a few dividends in the interim.

Best,

Lewis

Lewis

I agree S&U is a hidden gem and this writeup does it justice.

I also think it is worth at least £30-35. It doesn’t have good comps in the UK, Moneybarn’s valuation being obscured by the rest of PFG’s business. In the US, however, CACC trades at 2.7x book. CACC does similar ROCE to S&U but has debt to capital of 65% vs 35% for S&U. CACC’s book is riskier and is now facing much greater regulatory risk given the new Biden-appointed head of the CFPB is a Elizabeth Warren protégé. S&U also still has a lot of runway as use car lending is underpenetrated relative to new in the UK and used in the US, and the lender universe is very concentrated.

Another way I look at valuation: if we ascribed a notional 50% debt to capital to S&U which, given it underwriting track record, it could comfortably support, then its return on equity is around 30-35%, which when factoring in the growth in used car financing and the optionality around Aspen justifies 2-3x book, or £30-40.

There is a significant margin of safety here on a growing, quality business (and for me this is a long term hold, which I have had the opportunity to acquire at a very cheap price).

Some other points additive to your writeup:

• On your comments on their approach to entering new businesses, I would add they have also been good at exiting. They sold the heritage business, home lending, in 2015 at a very good valuation (2.5 or 3x book from memory) and with very good timing no doubt given what the regulatory tea leaves were telling them at the time. They also had a second mortgage startup before the GFC and were quick to shut that down when it didn’t seem a runner. They were also contemplating applying for a banking licence a few years ago but dropped the plan as they thought the regulation would be too restrictive – I could see many other management teams wanting the deposit base to significantly increase their loan book, but that’s not how the Coombs think.

• I agree with your sanguine view on regulation. My biggest concern has been the risk of them being targeted by Claims Management Companies (CMCs) as the payday lenders were, and more recently Amigo and the home credit providers, especially Provident. However, as you point out the FOS have not really upheld any complaints against Advantage, whereas they have been upholding complaints against Amigo and increasingly against home lending providers for relending. The FCA is most concerned about affordability and S&U has had only a few affordability cases, none of which have been upheld.

• Aspen is led by Anthony’s and Graham’s cousin, Jack, who has recently taken over his mother’s 14% stake.

Regards

Jerry

Jerry, thank you for the comment. You obviously know your stuff.

I agree CACC is one of the better comps globally, although I also agree that, between the two, I would have a very strong preference for SUS. The leverage at Credit Acceptance makes me nervous, they are much more penetrated in their market and they faced regulatory pressure even prior to the new Biden administration. The Massachusetts attorney general filed a complaint last year alleging that CACC was systematically misleading its borrowers. The UK regulatory regime makes me more comfortable than the US one does. They use auto immobilisers over there, heavily align incentives with the dealerships (which is a genius idea, but has some drawbacks), and broadly speaking the US view on borrower affordability seems to be that ‘if you can’t pay it back, it’s your fault and you should never have taken out credit in the first place’. For the more libertarian among us, that might sound fine, but it suggests to me that the likely direction of regulatory pressure for CACC appears is much less favourable than for SUS. And – as you point out – for all this you pay quite a significant multiple of book value.

I note that Anthony Coombs, in his recent interview with Proactive, was quite bullish about exploring new potential borrowing sources to finance the significant growth they see in the coming years. This is no real surprise given the pace at which Aspen is growing – much stronger than I had anticipated in the piece above, three months ago. This is likely to be positive for RoE in the medium-term, particularly if they can get their blended cost of debt down (which I hope is possible as they do more property bridging lending). I think it’s fair to say that S&U has a suboptimal financing structure from a valuation perspective.

Wholehartedly agree on the flexibility, particularly with respect to the home credit business and the challenger bank plans. I hadn’t actually realised they had tried a ‘mortgage startup’ – interesting, thank you.

And yes, regulation still the biggest risk. They do an excellent job of managing the ‘knowable’ risks – the two primary ones I consider being credit quality and how they treat their customers. I genuinely think they are a company that cares about customer outcomes above and beyond what is simply required by the regulation. My belief is that this should hold them in good stead, but in my view, the FCA acted with very heavy hands in the COVID pandemic and is liable to do so again, so I keep an open mind as to how the future may look.

Best,

Lewis